Fairness is vastly overrated. Whatever this overused and underdefined term may mean, it stands as the primary obstacle to meaningful tax reform. The intuitive emotional appeal that everyone ought to pay her/his “fair share” has come to change the nominal purpose of taxation from the effective financing of our democratically determined public purposes to the maintenance of some fuzzy ideal of equity. Ironically, using this feel-good “theory” of fairness to maintain a fiscal system based on a highly progressive personal income tax, an extremely narrow sales tax and a rigorously market-value property tax ends up, in practice, hurting most precisely those low-income households the “theory” is supposed to protect.

Consider what really happens in the fiscal sausage factory. First, legislators twiddle their thumbs until the (non-legislative) economic and revenue forecasting committees sift their tea leaves and tweak their equations to provide a number that becomes the size of the state revenue pie. Next, the governor and political parties spend several months arguing about how to slice that pie. Next, in the wee hours of some June morning, bleary-eyed members of the appropriations committee make the final cuts. And all the while, city and town officials struggle to set mil rates based on guesses about state aid and the hard reality of property values they cannot change.

Additional Photos

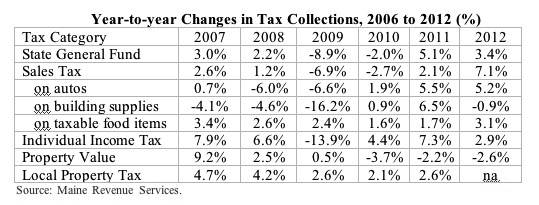

So how does “fairness” fare in this “system?” Consider the table above.

State General Fund revenues increased by 3 percent in 2007, slowed to 2.2 percent in 2008, fell off the table in 2009 with a drop of nearly 9 percent, fell another 2 percent in 2010 before jumping back by 5.1 percent in 2011 and 3.4 percent in 2012. In short, state tax revenues are volatile — tied to the up and down swings of the larger economy. And these swings are completely unrelated to the ongoing need to teach children, pay hospital bills, maintain roads and protect our citizens and our environment. How “fair” is that?

And the reason for this volatility? Precisely our dependence on the revenue streams most closely tied to economic fluctuations — individual income, auto sales and the construction industry. Gaze for a moment on these lines — drops of over 16 percent, nearly 14 percent and nearly 7 percent in one year, followed by jumps of 5 to 7 percent in subsequent years. Hardly a recipe for rational program administration.

Then look at the local property tax line — a drop from increases above 4 percent to between 2 and 3 percent following the collapse of housing prices, but nowhere near the swings seen in state revenues.

So what is the harsh reality of our “fair” taxation system? In a word, annual last-minute cuts to social services and a harsh (or sheepishly embarrassed) shrug of the shoulders to town managers and boards of selectmen across the state.

The only item in the list that is close to property tax revenues in terms of annual stability and predictability is the small portion of food items that are subject to the sales tax. And that line is precisely the clue we should see as the avenue to a stable, government program-supporting tax reform that will produce actual rather than theoretical fairness.

Charles Lawton is chief economist for Planning Decisions Inc. He can be reached at:

clawton@planningdecisions.com

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.