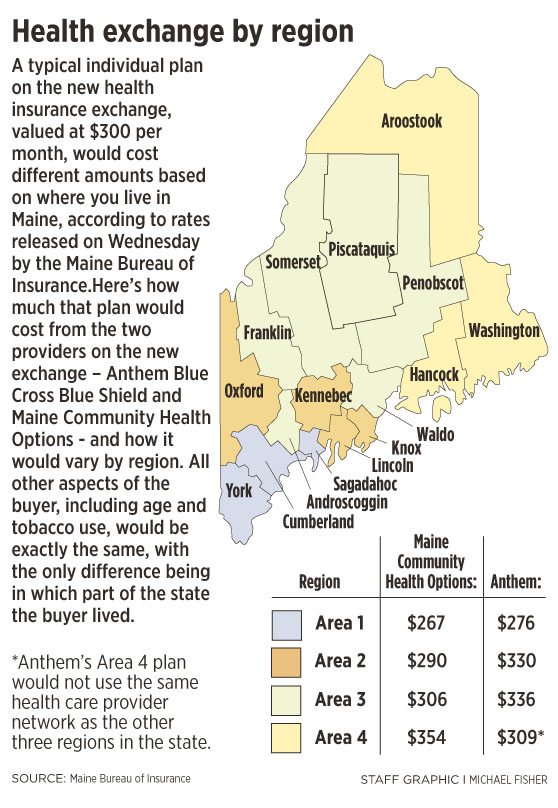

An Aroostook County resident who buys a health care plan on the new federal insurance exchange could pay $1,000 more per year in premiums than a Portland resident for exactly the same coverage, according to information released Wednesday by the Maine Bureau of Insurance.

The bureau released the rates that two participating insurance companies would charge for several types of coverage plans on the new exchange, set to go into effect Jan. 1 as part of the federal Affordable Care Act. Residents, mostly the self-employed or the currently uninsured, can begin purchasing insurance on the exchange Oct. 1.

Additional Photos

The rates released Wednesday must still be approved by the federal Centers for Medicare & Medicaid Services. And customers with incomes between 100 percent and 400 percent of the federal poverty level will be eligible for subsidies to help with the cost.

How much consumers pay will not only depend on how comprehensive a plan they choose, but also their age, whether they use tobacco and where they live.

One plan, valued at $300 if a buyer’s place of residence is not taken into consideration, would cost $354 a month in Aroostook County, but just $267 in Portland. The plan is being offered by Maine Community Health Options, one of the two providers on the new exchange. The other provider, Anthem Blue Cross Blue Shield, also charges different rates based on where a person lives.

Recent laws approved by the Maine Legislature have made it easier for insurance companies to charge different rates for customers living in different parts of Maine, said Joseph Ditre, executive director of the health care advocacy group Consumers for Affordable Health Care.

The insurance industry lobbied for the changes, arguing that it costs more to deliver health care in rural areas. The legislation made it easier to charge different rates based on which county a buyer lives in starting in 2011.

Before 2011, insurance companies were allowed to charge different rates based on county of residence, but in practice it wasn’t done because rates were based on a formula that took into account both a person’s age and where they lived, Ditre said. In practice, a buyer’s age was usually the dominant factor.

In 2013, the Maine Legislature passed a compromise bill that created four broad regions for which insurance companies could charge different rates for the same coverage, which replaced rates that varied by county. Plans offered on the insurance exchange will use the same four regions to determine geographic differences in rates.

But the compromise still leaves rural Mainers paying more for the same coverage than those in more urban areas in southern Maine.

Ditre – who unsuccessfully lobbied against allowing rates to vary by region – said residents shouldn’t be penalized because of where they live.

“Maine is a small enough state that we don’t need to do this,” Ditre said. “You ask yourself ‘Why?’ and the only answer you get is ‘because they can.’“

But Kevin Lewis, chief executive officer of Maine Community Health Options, said that one reason rates vary by region is because it costs more to deliver health care in rural areas.

“Geography is taking on a bigger role than before. But there are different underlying costs from area to area,” Lewis said.

For example, it takes longer for patients to get to a hospital in rural areas, which not only puts the patient at greater risk, but often makes the care more costly.

But Lewis said Maine Community Health Options, a new co-op offering insurance on the exchange, is working to eliminate some of the reasons why the costs differ by region. For example, the co-op will cover remote monitoring for patients with congestive heart failure and chronic obstructive pulmonary disease, which should help patients recognize problems and get to a hospital before symptoms progress far enough to require more costly care. The remote monitoring will benefit residents in rural areas more than in urban ones.

It remains unclear whether health insurance purchased on the exchange will cost consumers more or less than they would now pay on the open market because many details about the plans being offered have yet to be released. Plans offered on the exchange are set up differently than those now offered on the open market, Ditre said.

Ditre said he hopes the Bureau of Insurance will soon put together an easily understandable rate chart so people can better comprehend what they’re purchasing.

The bureau will be holding informational meetings in August to help people figure out how to purchase insurance on the exchange. Those meetings will begin at 6 p.m. at the following locations and dates:

• Aug. 15, University of Southern Maine, Portland.

• Aug. 16, Husson University, Bangor.

• Aug. 29, Central Maine Community College, Auburn.

• Aug. 30, University of Maine, Presque Isle.

Joe Lawlor can be contacted at 791-6376 or at:

jlawlor@pressherald.com

Twitter: @joelawlorph

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.