Bob and Jen Boylen want the year before college to be an exciting one for their 17-year-old daughter, Krista. But the couple’s own excitement is tempered by a nagging fear: that their daughter, a Gorham High School senior, will have to take on a significant amount of student loan debt that will interfere with her future happiness and success.

“I don’t think kids realize how much you have to pay back,” Bob Boylen said.

Additional Images

WHAT'S THE TRUE COST?

For students who are expecting to receive need-based financial aid, the price of a college’s tuition can be misleading. Many colleges with higher tuition fees also have a better track record of covering students’ financial needs with grants and scholarships, making them less expensive than they seem. Consider the following estimated out-of-pocket cost comparison between Bowdoin College and the University of Southern Maine, which assumes the student resides in Maine and has an expected family contribution (EFC) of zero (find our EFC estimator here). Student loans and wages from campus jobs (work study) are considered out-of-pocket costs. The comparison does not take into account any merit-based financial aid the student could receive.

Bowdoin

Yearly cost of attendance: $61,650

Average share of student need met: 100 percent

Cost of four-year degree: $246,600

Grants/scholarships: $235,787

Loans/work study: $10,813

Unmet financial need: $0

Out-of-pocket cost: $10,813

USM

Yearly cost of attendance: $19,036

Average share of student need met: 76 percent

Cost of four-year degree: $76,144

Grants/scholarships: $25,305

Loans/work study: $31,993

Unmet financial need: $18,846

Out-of-pocket cost: $50,839

Source: Collegedata.com

HOW TO CHOOSE A SCHOOL

Cost should not be the only factor in choosing a college, but it is an important thing to consider, experts say. Here are several things to look for when determining whether a college is likely to be affordable:

– A history of providing generous grants and scholarships, both need-based and merit-based

– A history of covering most or all student financial need

– A policy of not reducing grants and scholarships after freshman year

– A history of low student debt upon graduation

– High student retention and four-year graduation rates

One resource for determining a college’s financial friendliness is collegedata.com. Registration is free, but the website does require you to enter a name, address and email.

Source: Collegedata.com

But Krista Boylen said she does understand the need to keep her debt as low as possible. In her college search, she focused on less expensive schools in the Southeast and ultimately chose the University of Alabama. She’s also thinking about serving in the Peace Corps after graduation, which would reduce her college debt further.

“It’s not going to be easy for our family,” she said, noting that her parents’ income is too high for her to receive need-based grants but not high enough to pay for her and her three siblings’ college educations. “We’re not going to get financial aid.”

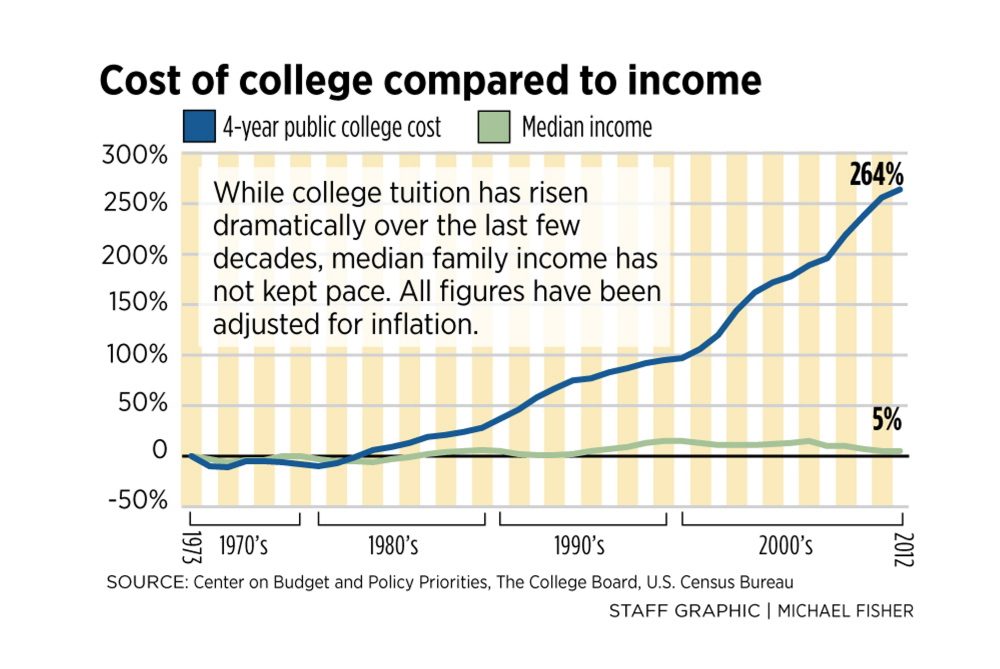

Awareness of the nation’s staggering $1 trillion in total student loan debt – higher than the total amount of U.S. credit card debt – has caused many students and their parents to approach the college application process as a cost-benefit analysis. They are thinking about how to get the best education possible for a reasonable price while taking steps to minimize the accrual of debt.

More students are choosing schools based on the institutions’ generosity in doling out financial aid. Some are attending a lower-cost community college for two years before moving on to a four-year college.

They are also using strategies for determining what amount of debt will be manageable, based on factors such as family finances and intended profession. Their goal is to get the best education they can actually afford.

Excessive college debt destroys graduates’ credit scores, delays marriage and children, and makes it impossible to buy a home or save for retirement. As a result, college students are seeking out ways to reduce the cost of their education through scholarships, grants, community college and work-study programs, or by joining the military or a public-service organization such as the Peace Corps.

But it can be difficult to think rationally during the anxiety-inducing college application process, which is opaque, confusing and complex, said consultant Gary Canter, who owns Portland-based College Placement Services.

Many students and their parents still think the priority should be gaining admission to the most prestigious, selective school that will have them, regardless of the cost, Canter said.

“The vast majority of parents will do anything for their kids, including committing financial suicide, or allowing their kids to commit financial suicide,” he said.

Drowning in debt

Seniors at U.S. public and private nonprofit colleges in 2013 graduated with an average of $28,400 in debt, up more than 12 percent from $25,250 in 2010, according to the nonprofit Project on Student Debt. Graduates from colleges in Maine had a slightly higher average debt of $29,934 in 2013, the seventh highest among all 50 states.

Among more than 100 college graduates in Maine with student debt surveyed recently by the nonprofit Maine People’s Alliance, more than one-third said they could not afford to make their monthly payments. The alliance is a grassroots organization that focuses on social issues and leadership development.

Many of the graduates complained of student loan payments that are nearly as high as a typical mortgage payment, and said their student debt has forced them to postpone buying a house, getting married, having children and even moving out of their parents’ homes.

Kimberly Hammill of Levant told the alliance that she amassed more than $150,000 in debt to pursue bachelor’s and master’s degrees in social work at the University of Maine in Orono.

“Graduating in 2008 at the peak of the recession meant that I wasn’t offered the income promised by a master’s degree,” said Hammill, who is a single mother. “My starting salary was what I had been earning when working as a bachelor’s holder.”

Hammill said paying for the education she was hoping would improve her and her daughter’s quality of life is now keeping her dependent on government assistance, just as she was before attending college. She said getting a second job was her only realistic option, despite the impact it would have on her ability to be a good parent.

“I shouldn’t have to make a choice between being active in my daughter’s life and putting food on the table,” Hammill said.

Another college graduate who took the survey, Jennie Pirkl of South Portland, told the alliance that she and her husband had accrued more than $100,000 in total student loan debt to obtain their master’s degrees.

Having so much debt severely restricts the couple’s ability to manage their finances and serve as foster parents, Pirkl said, despite the fact that they both have good jobs. She is a community organizer and he is a teacher.

“Even though we make what should be middle-class incomes, the reality is that we live in a state of financial insecurity because of our crushing student debt,” Pirkl said.

One problem Pirkl sees is that many jobs which require a graduate degree don’t pay well enough to cover the cost of obtaining one.

“Careers that require higher education should be able to provide the income necessary for people to pay off the loans used to fund that education,” she said.

Making the right choice

Despite the myriad student- loan-debt horror stories, Canter insists that the system is not fundamentally broken. The problem, he said, is that students and their parents often fail to think rationally when choosing a college.

“There is no such thing as a student debt crisis,” he said. “All there is is misinformed parents and kids who borrow more than they should.”

One of the most common mistakes is believing there is one college that’s the perfect fit for a particular student and his or her interests, Canter said.

In reality, any number of schools offer the types of education and experience a given student wants, he said, which means college applicants should focus far more on choosing the most affordable school among their potential choices.

“The notion of finding the ‘right fit’ is something of a myth,” Canter said.

College applicants should first establish a reasonable price range based on their family finances and expected income, and then look only at schools within that range, he said.

Canter disputes the commonly held belief that attending a prestige university such as Harvard or Yale opens doors to jobs and income levels that otherwise would not be attainable. At best, it might get you a job interview, he said, but you still have to earn the actual job.

“It’s a 15-minute advantage,” Canter said.

For students who know which career they intend to pursue, it is equally important to choose a price range for college that is in line with what a worker in that field is likely to earn, said David Leach, a public administration expert who recently authored a guide to student loans for the Maine Bureau of Consumer Credit Protection.

The Downeaster Common Sense Guide to Student Loans, available free on the bureau’s website, contains a table of average starting salaries and earning potential for various careers, along with the maximum student debt load workers in each field should accrue.

For instance, a graduate with a bachelor’s degree in accounting can expect to earn a starting annual salary of about $39,000 in Maine, according to the guide, and an experienced accountant has the potential to earn about $63,000 a year. Therefore, accounting majors should not accrue more than $36,500 in student loan debt if they want to be able to repay those loans comfortably based on their anticipated income.

It’s a new way of thinking about education that has become necessary because of the escalating costs, Leach said.

“I never gave it a thought about what I was going to earn,” he said.

Financial aid abounds

The best way to pay for college is to get others to pay for you, also known as financial aid.

Depending on the school, students whose families earn less than six figures are likely to receive some amount of need-based financial aid. If they have siblings attending college at the same time, they’ll receive even more.

The key to pricing a college is to calculate the difference between a student’s financial need and the amount of need the school typically covers. Financial need is defined as the cost of attending a college minus the expected family contribution, commonly known as EFC (find our EFC estimator here).

The EFC does not necessarily represent what a family actually can afford to contribute. It is merely a calculation colleges use to determine how much financial aid they should provide a student.

Canter said the EFC is generally 15 percent of the family’s annual gross income, plus 5 percent of its non-retirement assets, plus 30 percent of any savings in the student’s name.

Krista Boylen completes homework in her bedroom in Gorham last month. The high school senior is looking hard at tuition costs as she selects a college. Her parents, Jen and Bob Boylen, will assist with some of the tuition bill and the also expect to help three other children who also plan on attending college. Jen and Bob Boylen said they hope their daughter will make a school choice based upon both a feeling and financial perspective, but because their other children will also likely attend university, they know it will be difficult to pay four children’s tuition bills outright.

So a family that earns $75,000 a year, has $50,000 in non-retirement assets and a $5,000 college savings account for the student would have an EFC of roughly $15,250 per year. Need-based aid would not cover that amount but may cover everything else, depending on the school.

For the Boylens, who own and operate an insurance agency in South Portland, their estimated EFC for 2015 is $39,000. But they can’t actually afford to contribute anywhere near that much, Jen Boylen said.

“That’s not reality,” she said.

Two tips for financial aid are to apply as early as possible in January of each year the student attends college, and to be aware that a college’s financial aid award can be appealed if it falls short of the student’s need by $10,000 or less, the experts said.

“What we know about financial aid is the earlier you apply, the more you get,” said Doug Drew, a guidance counselor at Portland High School.

The other key form of financial aid is scholarships, said Cherie Galyean, education and scholarship manager for the Maine Community Foundation.

There are three basic levels of scholarships, she said: local, state/regional, and national.

Local scholarships reward students for attending college in their own communities, Galyean said. High school guidance counselors are a good source for learning what local scholarships are available, she said.

State and regional scholarships are awarded by a variety of organizations that may be looking to help students with particular interests or abilities, Galyean said. For a list of such scholarships in and around Maine, students can visit the Community Foundation’s website, mainecf.org, and the Finance Authority of Maine’s website, famemaine.com.

National scholarships are more difficult to obtain, Galyean said, but they are often quite lucrative and therefore worth the effort. They can be found in searchable online databases such as fastweb.com and scholarships.com.

“Those are more of a crapshoot, but they’re definitely worth looking for,” she said.

Canter said it is best for students to think of the scholarship application process as a job. Even a smaller scholarship for $500 is worth the time and effort to apply if the process is broken down into an hourly wage, he said.

“That’s $500 for about an hour’s work,” he said.

Other ways to pay

Some students help pay off or reduce their student loans through other means, such as starting off at a community college, working on or off campus, or joining ROTC, the military or a public service organization such as the Peace Corps, the experts said. Under the Post-9/11 Veterans Educational Act of 2008, any student who has served at least three years of active duty in the military since 2001 can receive full reimbursement of his college costs for up to four years. College graduates also can request full forgiveness of their federal student loans after making payments for 10 years if they have worked for a public service organization such as the Peace Corps.

Leach said that in general, starting off at a lower-cost school such as a community college has no negative impact on a student’s academic record and can reduce the cost significantly.

“Many students choose a lower-cost solution for their first year or two and then transfer to their ‘first choice’ school with 15-30 ‘discounted’ credits,” Leach wrote in his Downeaster student loan guide. “This can greatly lessen your overall student loan debt, as well as strengthen your application to your first choice school.”

However, Leach cautioned that the student should check first to ensure that all credits are transferable between the first and second college.

“If the school does not accept the transfer credits, you will end up paying twice for the same class,” he said.

The Boylens say they have done what good parents are supposed to do. They’ve pushed their daughter to achieve excellent grades. They’ve helped her come up with a reasonable list of potential colleges and socked away $10,000 into a 529 college savings plan to help her cover the costs.

Still, that amount won’t come close to covering the cost of Krista’s higher education. And their EFC is likely too high for her to receive need-based aid. At the University of Alabama, the estimated cost of attendance for an out-of-state student is about $39,000 a year – exactly the same as her family’s estimated EFC.

That means she would have to pay the full retail price unless she receives merit-based scholarships.

Krista has a sister who is a high school freshman and twin 10-year-old brothers. The Boylens said they want to be fair to all four children, which requires them to set limits on how much help they can provide. As a result, they plan to help all of their kids seek out quality schools that don’t charge exorbitant tuition fees.

“Essentially, we’re looking at 11 straight years of college,” Jen Boylen said.

From now until next fall, Krista will be applying for merit-based scholarships and thinking about the type of career that would help make her student loan debt affordable. Her current plan is to study political science and international business.

“I would love to be a history teacher, but you don’t make a lot of money,” she said.

This story was updated at 10:12 a.m. on Monday, Dec. 8 to correct the spelling of Cherie Galyean’s last name.

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.