Just as Social Security and Medicare benefits were dangled above the shredder in the debt-ceiling debate, another of Washington’s sacred cows could end up on the chopping block soon.

The mortgage interest deduction, which allows 35 million homeowners to write off their mortgage interest payments, may be in for serious restructuring if ongoing efforts to pare the bulging federal debt are broadened.

Additional Photos

As part of the just-concluded debt-ceiling debate, a bipartisan group of senators known as the “Gang of Six” proposed lowering the limit on mortgages eligible for the deduction from $1 million to $500,000 and restricting the tax break only to primary residences.

But as it has through decades of federal budget cuts and crises, the popular provision emerged unscathed in the debt-limit compromise that President Obama signed into law Tuesday. That reprieve, however, may not last.

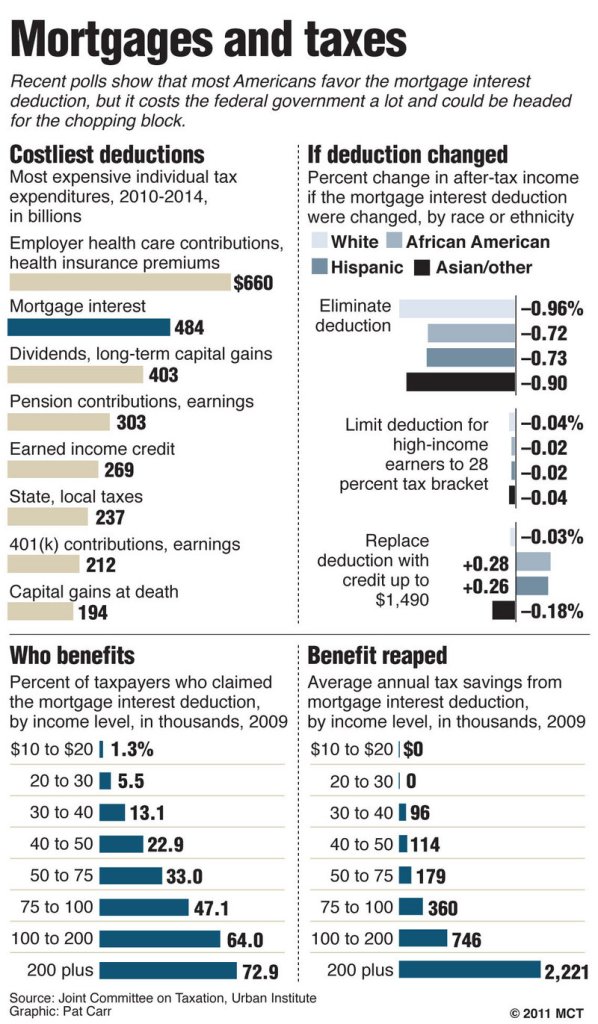

With lawmakers looking for $1.2 trillion to $1.5 trillion in additional budget cuts by the end of the year, the deduction — which will cost the federal treasury about $131 billion next year — makes for a juicy target.

First of all, the revenue the government forgoes because of the deduction is huge — more than twice the entire budget of the Department of Housing and Urban Development. And there are better, more cost-efficient ways for the tax code to encourage homeownership, economists argue. Plus, the benefits of the deduction go disproportionately to the upper middle class, whose bigger homes and mortgages bring bigger tax write-offs.

In fact, the average value of the deduction increases with income, from $91 for those who make less than $40,000 a year to $5,459 for those who earn more than $250,000, according to a 2010 report by the Tax Policy Center, a joint project of the Urban Institute and the Brookings Institution, two center-left research centers.

For most homeowners who take the deduction, the tax savings it provides doesn’t make the difference between owning and renting. It simply helps them afford more expensive homes.

Housing advocates have long argued that if homeownership is the provision’s goal, a refundable tax credit for all taxpayers would be more effective.

“If we wanted to increase homeownership, we’d target the incentives toward the families who are on the margins of possibly not being able to afford to own a home. … It’s pretty clear that’s not what the mortgage interest deduction does in the way it’s currently designed,” said Seth Hanlon, the fiscal policy director at the liberal Center for American Progress.

The idea of curbing the mortgage tax break has been around for years. President George W. Bush’s tax overhaul panel recommended limiting the deduction in 2005, but the issue quickly disappeared as lawmakers showed no stomach for it.

The Great Recession may have changed that, however. As federal revenues plummeted, calls to trim and revamp the deduction have come from the Bipartisan Policy Center’s Debt Reduction Task Force and Obama’s National Commission on Fiscal Responsibility and Reform.

“While nothing has happened in response to any of these ideas, it is definitely now on the table as it has never been before,” said Eric Toder, a co-director of the Tax Policy Center.

So don’t be surprised if the deduction is back on the carving table just in time for Thanksgiving, when a new 12-member bipartisan debt-reduction legislative committee created by the debt-ceiling compromise must recommend even more budget cuts.

At an estimated cost of more than $484 billion from 2010 to 2014, the mortgage deduction is second only to the employer-paid health insurance exemption as the nation’s most costly individual tax break, according to the congressional Joint Committee on Taxation.

Many want some of the tax savings from the mortgage deduction to address the housing needs of low-income renters and buyers.

A new study by the conservative Reason Foundation suggests eliminating the deduction altogether in order to fund a revenue-neutral 8 percent cut in federal taxes for everyone. Currently, only about 25 percent of taxpayers benefit from the mortgage interest deduction.

Only taxpayers who itemize can claim the deduction, so only about 30 percent of filers typically take it each year. Lower-income people are less likely to itemize.

“The deduction is used almost exclusively by people in the top income brackets with large mortgages. Renters, along with lower- and middle-class families, are getting a raw deal. Taxpayers and the economy would be best served by ditching the mortgage deduction and lowering overall tax rates,” said Anthony Randazzo, the director of economic research at the Reason Foundation and a co-author of the report.

Lawrence Yun, the chief economist at the National Association of Realtors, said that now would be the worst possible time to tinker with the deduction because it would further depress demand in the struggling housing sector. Any reductions would most hurt younger families, who typically have higher amounts of interest on their mortgage balance sheets, Yun said.

He said that eliminating the deduction would amount to a tax increase on the middle class and would lower property values by 15 percent. Others project that without the deduction, property values would fall anywhere from 2 to 12 percent.

Rather than eliminating the deduction altogether, Hanlon and the Center for American Progress have proposed gradually stepping down the value of the deduction over a 20-year period until it becomes a flat 15 percent tax credit that’s available to all households.

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.