The good times are here, if Michael Dolega is right.

Dolega, senior economist for TD Bank, says 2015 will be the best year of economic recovery from the 2007 recession, both for the country as a whole and for Maine.

Additional Images

Job growth will pick up and the economy will grow, he told those attending the Maine Real Estate and Development Association annual meeting Thursday. But the rate at which Maine businesses will add jobs and see economic growth will only be about half that of the U.S., he said.

Dolega said the country is poised for solid economic growth, even as Europe and Japan teeter economically. He said low energy prices, because of falling oil prices, and continued low interest rates on loans will help propel economic growth.

Maine’s economy is expected to grow about 1.7 percent this year, a little more than half the rate he expects for the U.S. as a whole. And, he said, Maine employers are expected to add 7,000 jobs this year – a growth rate of about 1 percent that again is half what is expected nationally, but the best performance since 2000.

In real estate, which is what brought most of the 1,000 or so people to the Holiday Inn by the Bay on Thursday, Dolega said the outlook is also good, but not quite so robust.

He said that while real estate prices didn’t fall as far in Maine when the housing bubble burst in 2007, that means the recovery has been slower.

“There’s less upside momentum,” Dolega said. But mortgage rates are forecast to remain low, meaning the housing market in Maine should continue to recover. In individual real estate sectors, industrial real estate in southern Maine is particularly strong.

Justin Lamontagne, a commercial real estate broker at NAI The Dunham Group, said he’s never seen a space crunch in the industrial real estate market like the one Greater Portland is experiencing now.

The region – defined as Portland, South Portland, Westbrook, Gorham, Scarborough, Saco and Biddeford – has a vacancy rate of 4.12 percent for industrial real estate, which Lamontagne said is “ridiculously low.”

That number has dropped consistently over the past few years; it was 7.86 percent in 2011. Historically, the vacancy rate for this sort of real estate is somewhere between 8 percent and 10 percent, he said.

Lamontage said the current vacancy rate is so low he thinks there’s no way it can keep falling, and he predicted Thursday that it will rise in 2015.

“They have to, right?” he said, immediately doubting his own prediction. “But if we come back next year and it’s 3 percent, I won’t be shocked.”

HOSPITALITY

The hospitality sector is likewise expected to do well in 2015, even though a large number of hotel rooms was added to the Portland market in 2014.

More than 660 new hotel rooms have been added to the Portland market in the past year. But Daren Hebold, president of LUX Realty Group, said he’s not worried that the city will have more rooms than tourists to fill them.

High-end brand-name hotels, like the new Hyatt Place in the city’s Old Port, have a following, and Hyatt fans will travel here to spend their hotel award points, he said.

Moreover, there’s been a shortage of rooms in the city’s downtown, an increasingly popular destination because of Portland’s vibrant restaurant scene.

“The new hotels are going to bring new demand,” Hebold said. “The market will absorb them, given the growth in tourism.”

There are four new hotel projects in the city: the Westin Portland Harborview, the Marriott Courtyard, the Hyatt Place Marriott and the Press Hotel, which is scheduled to open this spring.

In the audience, Tim Soley, whose 130-room Hyatt Place opened last May, said his hotel earned a profit last year, a benchmark that new hotels usually take a few years to achieve.

Statewide, new hotel projects totaling 879 rooms are in the planning or construction phases, which will increase room supply by 2.4 percent, Hebold said. Occupancy levels will remain flat this year given the inventory of new rooms, he said, but average room prices will increase by 2.5 percent, to roughly $119 per night.

RESIDENTIAL

Echoing much of the optimism seen in other real estate sectors, presenters for Maine’s residential markets also saw encouraging trends.

In the multi-family sector, Brad Vitalius, owner of Vitalius Real Estate Group, said inventory in Greater Portland is especially tight. There are only 34 multi-family units on the market now – there are typically 80-100 units, he said. And demand, driven primarily by investors who entered the market in 2014, has driven the typical sale price of $60,000-$65,000 per unit to $80,000-$100,000 this year.

Munjoy Hill is the epicenter of that interest, said Vitalius, but that demand is creating a ripple effect in other neighborhoods outside the Portland peninsula.

“The peninsula is so dense that location doesn’t matter as much as it used to,” Vitalius said.

Most metro areas outside Portland were also seeing increases in sales volumes of multi-family buildings, especially compared with the bottom of the recession in 2009. In the five years since, sales volume of multi-family buildings in Portland has grown 123 percent; South Portland 193 percent; Westbrook 56 percent; and Saco-Biddeford 103 percent. Only Lewiston-Auburn saw a decline, with sales volume dropping 12 percent from 2009 to 2014.

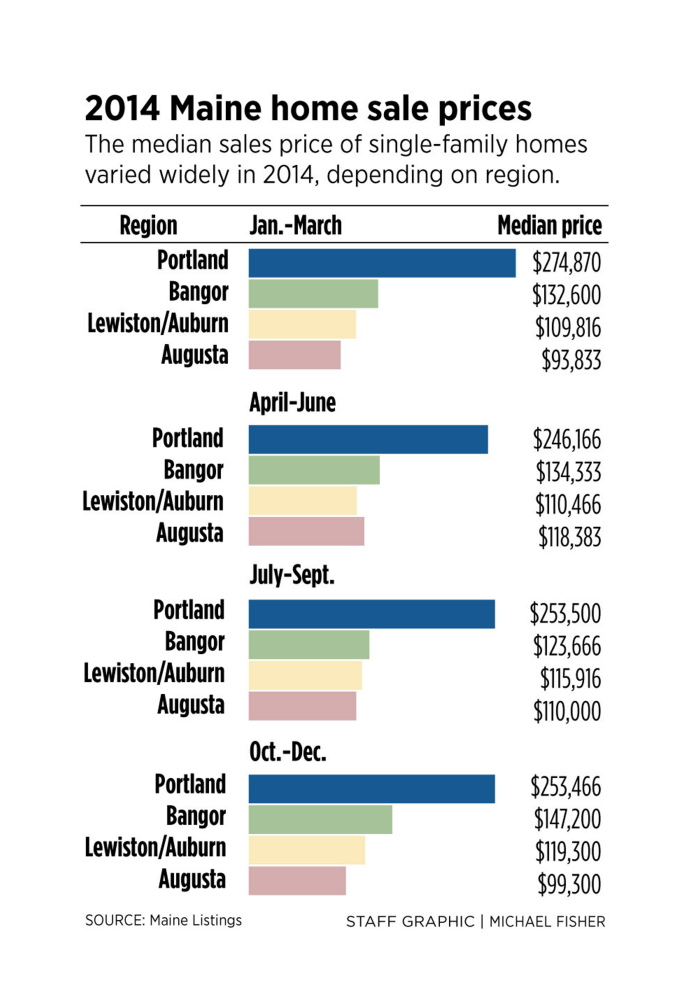

Portland was also the outlier in the single-family home market. While all the other metro areas reported a mix of sales and pricing trends, Portland-area homes were selling in 2014 at twice the price – and sometimes more – as houses elsewhere in the state.

Presenter Angelia Levesque of Better Homes & Gardens/The Masiello Group, said uncertainty around jobs in the rest of the state is causing uncertainty in the housing market and holding back sales. She also attributed high student debt load and a misunderstanding about home financing as drags on Maine home sales.

“Many young people think 20 percent down payment is needed,” she said. “The lenders and Realtors in the audience … we have some work to do.”

RETAIL

Retail prognosticators who predict Amazon will be the death of bricks-and-mortar stores haven’t taken a look at the data Mark Malone, co-owner of Malone Commercial Brokers, shared with the audience. Malone said online sales represented only 6 percent of the $4.5 trillion spent on purchases nationally last year. He offered a comparison between Amazon and Walgreens, both of which reported sales of $75 billion in 2014. But Walgreens reported $2 billion in profit, while Amazon reported $274 million.

Malone said retailers who have blended technology into their physical stores are succeeding, and pointed to the Yarmouth Hannaford supermarket as an example of click-and-collect shopping that is catching fire nationally. Shoppers place and pay for their orders electronically, then drive up to the store to collect the purchases waiting for them.

Overall, Greater Portland’s retail sector is strong, with vacancy rates running at about 3.6 percent versus the national average of 9.7 percent. Malone said there’s been some notable shuffling of retail tenants from one property to another, mentioning that HomeGoods, Marshalls and Bob’s Discount Furniture are likely to leave their Clark’s Pond retail center in South Portland and relocate to Scarborough Gallery by the end of the year.

Outside of Portland, shoppers can prepare for an influx of discount dollar and Goodwill stores. Through 2015, 22 new stores will open, Malone said, bringing the statewide total to 132 stores geared toward bargain hunters.

Staff Writers Tom Bell and Whit Richardson contributed to this report.

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.