During the early days of the pandemic, it became clear just how important the industrial market is. Many essential businesses are industrial in nature—food production, distribution, utility and manufacturing companies needed to stay open and operating to allow larger groups of people to stay home and quarantine safely.

As everything we know as “normal” has changed, the Greater Portland industrial real estate market was a welcome oasis of continuity. For the sixth consecutive year, our overall vacancy rate was below 4 percent. In fact, when we pulled the data in December, our overall rate was a paltry 2.44 percent.

This sector now projects stronger than ever largely because of the challenges the pandemic has wrought. A variety of industrial end-users have grown in direct response to pandemic-related conditions: manufacturers on-shoring jobs, warehousing of Personal Protective Equipment and supplies and life science companies working on COVID-related testing and treatment supplies.

Of course, this pandemic is truly unlike anything any of us has ever gone through. It is irresponsible to simply say that the industrial market is immune from all the negative effects of COVID-19. There very well may be impacts coming that we have not even considered nor imagined.

That said, all the economic indicators we track suggest a vibrant year. The turbulent world events around us continue to foster the importance of domestic production, storing, and shipping of goods and materials. We say, for better or worse, bring it on, 2021!

MARKET TRAJECTORY

Despite a complete shutdown of industrial transactions during the spring of last year, the overall industrial slowdown was short compared to other “non- essential” markets like retail and office. Indeed, by the close of the year, most of our economic indicators including lease rates, sale pricing, cap rates, and overall inventory counts suggest an improving market.

Vacancy rates ticked up slightly from last year’s 1.84 percent to today’s 2.44 percent, but there are a handful of larger vacancies inflating that number. My sense is we’ll be working in a 2 percent vacancy environment for most of 2021. That is an inhibiting number for tenants, particularly small to medium sized companies in the 5,000 to 10,000 SF range.

Like the residential market, Maine industrial has been fiercely competitive. Virtually every industrial sale in 2020 set a record for its area, including Gorham which saw a $100/SF sale for a 14,000 SF building and Riverside Street which saw a $120/SF sale.

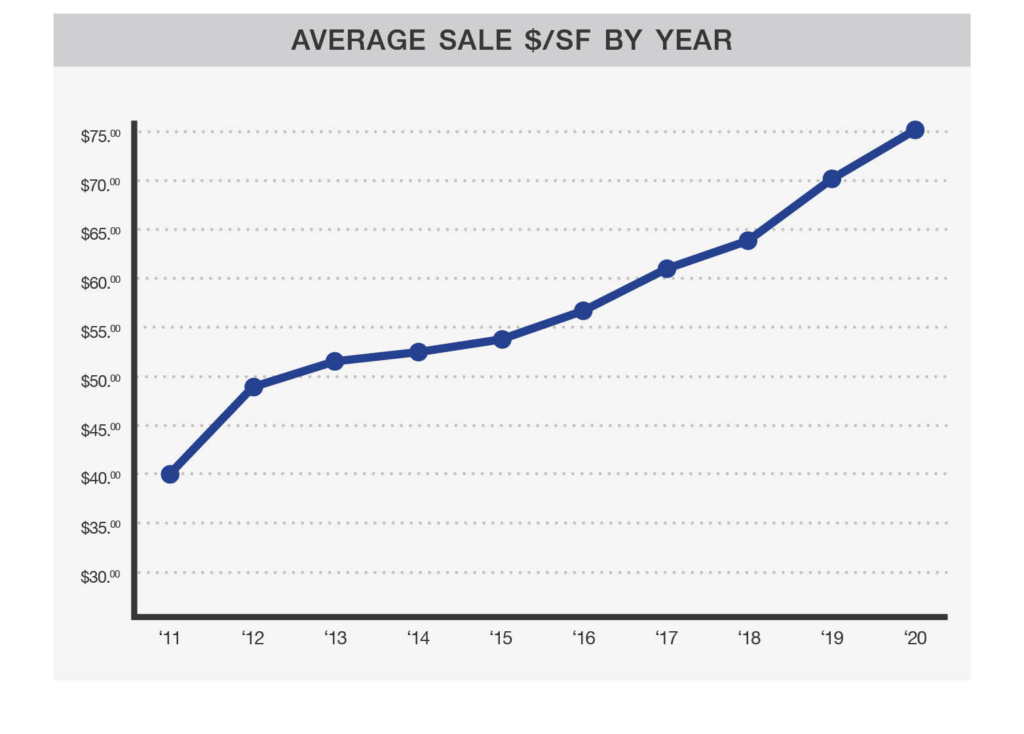

Overall, we are averaging over $75/SF, but that’s statistically deflated due to some larger SF sales. Anything under 20,000 SF is now easily in the $80-100/SF range. Premium sales are much higher, not to mention the low-cap investment sales highlighted herein. These are staggering numbers, nearing full replacement costs.

Speaking of investments, the capital market has never been hotter. We are now regularly seeing 7 percent cap rates for well-located, Class-A and B facilities, if not lower. Investors’ appetite for risk continues to increase with shorter lease commitments, shakier tenants and expanding geographics. These deals are often precipitated by 1031-Exchange and cash buyers driving competition. Banks and appraisers are starting to catch up and underwriting problems seemed to have eased. There is no doubt that financial institutions feel as comfortable with industrial real estate as they do with housing and multi-families.

With larger, institutional competition discovering our market, many smaller, local investors are on the sidelines. But opportunities remain for those who are well plugged into the market. A number of the more successful investment sales of the year were off-market local deals, and that trend is likely to continue into 2021.

VACANCY RATES

Greater Portland has had a six-year run of consistent 1.5 to 3 percent total vacancy. That’s challenging for tenants, but it also suggests we’re not overwhelmed with demand and could answer why so many developers remain hesitant to produce speculative industrial space.

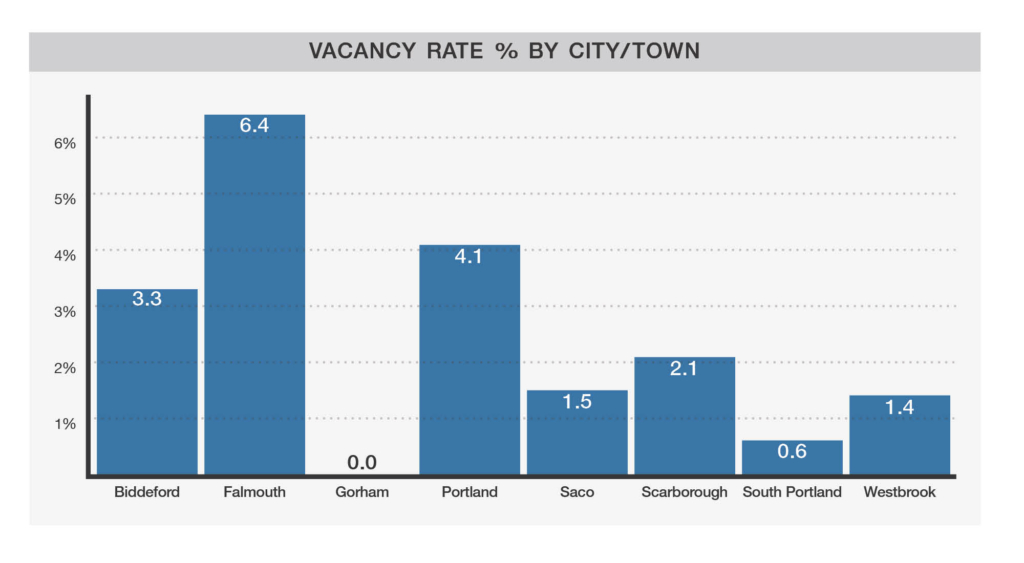

Still, entire municipalities are fully leased, like Gorham is for the second year in a row. Falmouth has a small, but potentially growing industrial market, with great location opportunity on both I-95 and I-295. But industrial zoned land is limited and would require municipal cooperation to increase those opportunities. Falmouth’s “high” vacancy rate of 6.4 percent is made up of only two available units in one building totaling 8,600 SF.

Saco and Westbrook industrial markets have stayed healthy. Their parks share some common traits: newer inventory, extremely quick and easy access to the highway, cooperative and supportive city governments, public utilities, and large, growing swaths of industrially zoned land.

Scarborough’s inventory stands to increase with the success of the Innovation District development at the Downs. Abbott Labs, one of the top growing industrial tenants in the market today, is based here, though their largest acquisition this past year (126,000 SF) was in Westbrook at 5 Bradley Drive.

LEASE RATES

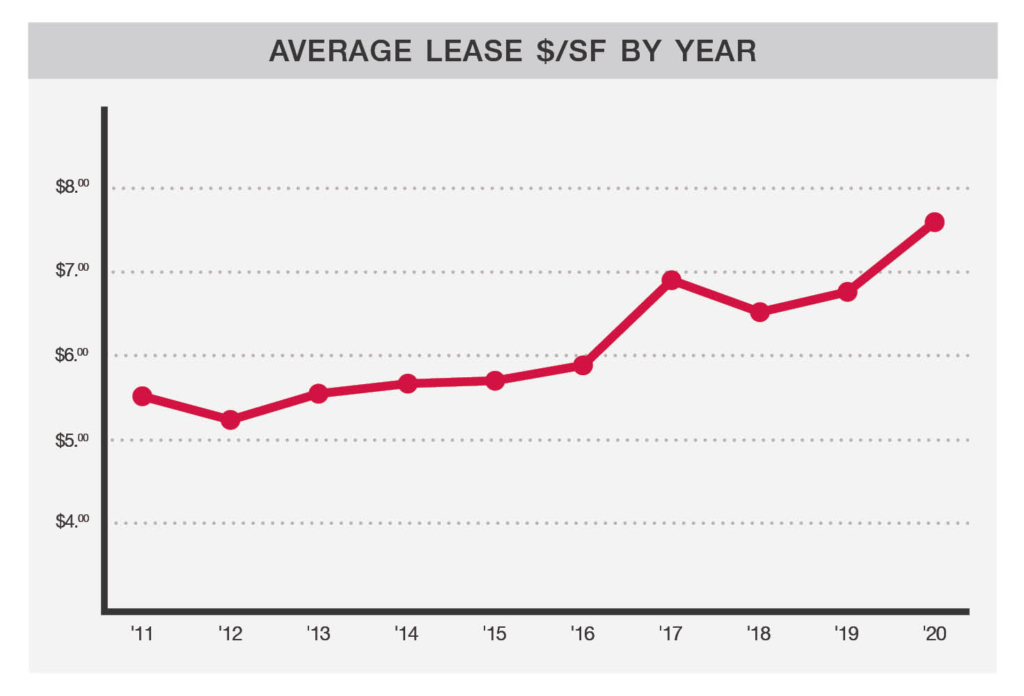

Lease rates increased dramatically in 2020, up nearly $0.90/SF to a market-record average of $7.65/SF NNN.

Anecdotally, we are hearing the historically long “landlord’s market” has emboldened many property owners to push the limits on rate increases. Until tenants push back or can come up with alternatives, there are no signs of this trend changing.

One alternative to high-priced existing inventory is even more expensive new construction. There are a number of developer-led industrial build-to-suit opportunities on the market today. But their pricing will likely be north of $10/SF NNN, if not higher. We hope that as the price gap continues to close between existing and new construction, the pace of new construction should increase.

Our best advice for tenant-clients remains, first and foremost, to be patient. But, at the same time, stay nimble and aggressive enough to strike at the next opportunity. Flexibility and creativity may be required as well, both in terms of location and asset quality or even classification. The repositioning of big-box retail into industrial is a trend we are watching closely and will likely add some much- needed inventory in the coming years.

NAI The Dunham Group is a commercial real estate brokerage company located in Portland, Maine. For over 45 years, The Dunham Group has provided in-depth, commercial real estate knowledge, market specialization, and proven representation to our loyal client base.

Read the entire Survey at dunham-group.com.

Comments are not available on this story.

Send questions/comments to the editors.