The commercial real estate industry has come to realize that the pre-COVID-19 pandemic capital markets for new construction and “value add” acquisition financing has tightened up. The debt funds and private equity firms that were hyperactive before the pandemic are now more selective on asset class, geography and, more importantly, leverage.

Gen X Capital Partners is a boutique real estate investment banking firm, closing on average more than $100 million a year in debt/equity placement and investment. We use the traditional platform of 65/35 to 70/30 (and occasionally 85/15 with a “stretch senior”) under typical debt/equity structures for essentially all asset classes. We push the leverage envelope a little further for a multi-family.

Once COVID-19 hit, however, those ratios nearly inverted due to debt funds, private equity firms and our Family Office partners pulling back their financing reigns. It became nearly impossible for sponsors to complete a deal without pouring in more personal capital, watching their cash-on-cash and IRR ratios drop substantially.

Enter the 99-year ground lease financing platform, also referred to as “land bifurcation,” a potential game changer for how we finance deals moving forward.

Think about it: the asset itself returns a 15%+ return on equity (ROE) per annum, while the land never generates more than a 5% ROE. It is simply a placeholder for the building, period. By separating the two, you can maximize overall returns without being dragged down by the low risk, low return land component.

Under this model you take what was a 5% ROE with the land, extract its cash value through a sale, reinvest it back into the higher revenue generating asset that’s earning 15% or more, then pay the 4% to 5% ground lease rate while unlocking a 10% ROE differential that was hidden in the dirt. Literally. And this is before you take into account the fact you can write off these lease payments along with your other deductible expenses, further elevating cashflow and IRR projections.

HOW IT WORKS

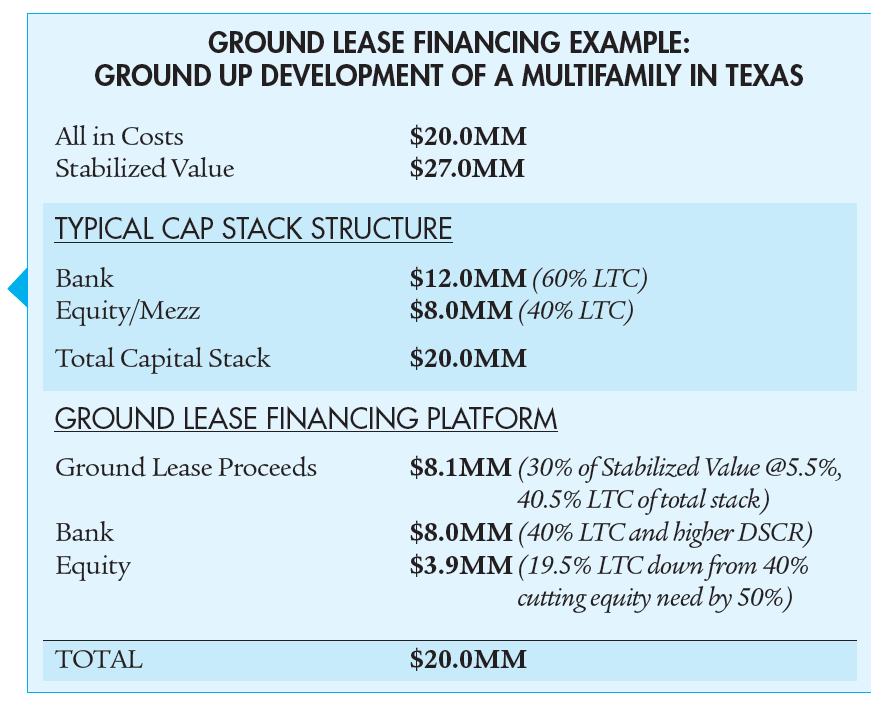

With a ground lease financing platform, we can bring in 4.25% to 5.5% capital (more on the rate differences later) that can solve from 40% to 50% of your LP equity need while driving down the banks LTC (Loan To Cost) and overall exposure and driving up their debt service coverage 20-50 BPs (Basis Points) or more, giving their loan coverage more strength.

Through the ground lease financing platform, our Family Office partner fund essentially acquires the land at 30% of projected stabilized value and these funds now became part of the overall capital stack. We then lease the land back to the developer at 4.25% to 5% depending on asset class, which is paid quarterly, and comes with a buyback provision that gives the leasehold lender (mortgage holder of the building structure) assurance that they can step in and cure any defaults. Additionally, in almost all cases we bring the leasehold lender, essentially making it a one stop shop, financing both sides of the transaction. More importantly this ground lease is in full compliance and accepted by HUD, Fannie, Freddie and all major lending institutions.

In the example to the right, the developer eliminated the need to raise $4.1 million in expensive LP/Pref/Mezz financing, keeping that in his pocket, and the he covered that difference at a 5% interest rate while jacking up IRRs. That expedited their development timeline since they are not bogged down raising capital, all while making the loan safer for the bank from a Debt Service Coverage Ratio (DSCR), as it typically increases 25 BP to 50 BP over that of traditional structure. We see this as a win for all involved.

Now, while there are a handful of great groups out there funding ground leases, keep in mind that not all structures are alike and the differences can be telling to the leasehold lender and the sponsor-developer. You may get quotes from 4.25% to 6%, but that spread comes with a price and that price is your ability or inability to exit the ground lease based on your timing needs. Almost all ground lease structures nowadays are 99 years and the ability to get out of one begins at year 30 or in some cases not at all unless you are willing to pay a hefty premium. You may be getting attractive 4.25% money but the ability to react to an opportune sale gets bogged down if you cannot offer up a fee simple transaction.

On the other hand, our fund offers a “buy back” provision with only a three-year rate guarantee, whereby we come in with 4.25% to 5.5% of funding, cutting a check for the dirt at closing based on 30% of stabilized value. This considerably drives down your equity need and by year three, you have the ability to take us out based on a very reasonable, pre-determined formula that allows everyone to make money. More importantly, this buyback provision gives the leasehold lender comfort knowing that if the sponsor were ever to default, they can step into their shoes, assume the ground lease, buy it out and now have a fee simple asset they can sell quickly. On the flip side if you default with your ground lease payments and we have to foreclose, the leasehold lender is notified allowing them to step in, cure the default, take over and sell the asset.

This can be done for all asset classes for ground up and “Value Add” projects with typical ground lease check sizes ranging from $2.5 million up to $200 million, in some cases. Can you use a ground lease financing mechanism on portfolio acquisitions that involve more than one asset? Yes. GenX Capital Partners is set to close on a multi-asset senior living portfolio (with HUD takeout) where we came in and solved for all of their preferred equity under our ground lease platform and, in the process, juiced their IRRs substantially. We simply close on the first asset and replicate the paperwork and legal structure for the remaining properties allowing utilization of economies of scale.

The ground lease financing platform could very well be the wave of the future in terms of solving for the tightened capital markets post COVID-19 pandemic. It won’t, however, come without its hurdles and one hurdle will be getting your lender comfortable with a 99-year ground lease ahead of them. But once they have had a chance to understand the structure, their ability to cure any defaults and then model the proforma to fund the loan has become stronger in terms of DSCR, the lender will become much more receptive. However, keep in mind that GenX Capital Partners has the ability to bring both the ground lease financing platform and the leasehold financing structure, allowing the sponsor a one-stop shop solution for their capital needs and most importantly, higher returns.

For more information on financing your project utilizing a ground lease platform or to have us model out what it would look like based on your current structure, contact Mark McClure at 305-507-6777 or Mark@GenXCP.com.

Comments are not available on this story.

Send questions/comments to the editors.