Sam Bankman-Fried, co-founder and chief executive officer of FTX, in Hong Kong on May 11, 2021. Lam Yik/Bloomberg

WASHINGTON – The sudden collapse of one of the world’s largest cryptocurrency exchanges rattled the nation’s capital this week, as lawmakers grappled with the wide-ranging fallout – and began to confront the consequences of neglecting the surging financial sector.

Only a few weeks ago, top Democrats and Republicans alike had been cashing campaign checks and working side-by-side with the vanguards of the industry, including FTX founder Sam Bankman-Fried, as they labored to craft new regulation in the frenetic, cutting-edge digital space.

Instead, Bankman-Fried unexpectedly became a potential case study of the costs of congressional inaction. While Washington dithered, he appeared to place a series of risky bets that incinerated his own fortune, jeopardized billions of dollars in Silicon Valley capital, threatened smaller investors and upended an entire ecosystem of cryptocurrency start-ups.

In response, investigators in the United States and abroad have opened probes into Bankman-Fried and his holdings. The Treasury Department has quietly placed calls to other large crypto exchanges to assess the risks of a broader contagion. And a slew of congressional committees have readied their own reviews, including a House inquiry announced Wednesday that could see Bankman-Fried testify under oath next month.

In the process, federal policymakers have been left to ask themselves a familiar, if uncomfortable question: Could they have prevented a crisis if they had paid close attention sooner?

“Over the years, the regulators … sorta invited them in, these crypto companies, and we’ve seen the damage they’ve caused,” said Sen. Sherrod Brown (D-Ohio), leader of the Senate Banking Committee.

Brown called for comprehensive cryptocurrency legislation, something that Congress repeatedly has proposed as the sector grew, yet time and again has failed to achieve in the face of staunch industry lobbying. In that time, a wide array of crypto firms have experienced meteoric rises – and once-unfathomable collapses – on the promise of great wealth that didn’t always materialize.

Still, Brown remained bullish that Congress could rein in cryptocurrency companies that have put investors large and small at risk: “They need to be held accountable.”

In some ways, the tumult around FTX tells the story of a Capitol often outpaced by the deft technology giants ostensibly under its watch.

From the burst of the dot-com bubble at the turn of the millennium to the rampant privacy mishaps at Facebook decades later, federal policymakers historically have been slow to anticipate the troubles of the digital age. Only after massive, costly scandals have lawmakers and regulators been stirred to action, sometimes with less-than-desirable results.

The nascent world of cryptocurrency – where digital tokens replace dollars, investments and payments, all without the need for traders, governments or banks – has presented perhaps the most complicated challenge to date. As an entirely new financial system has come online, Washington has been forced to choose whether to institute stringent rules on crypto or stay out of Silicon Valley’s way.

The U.S. government largely has adopted the latter approach, much to the relief of crypto companies, executives and investors. That has enabled the rapid growth and soaring valuations of bitcoin, a wide array of related currencies and an entire ecosystem of firms to support them. Until recently, that included FTX, a marketplace for buying and selling tokens that boasted its own currency – an exchange that at its height was the third-largest in the world.

But the peril of that approach came into sharp relief as FTX began to unravel. Questions about its finances – and whether Bankman-Fried used FTX deposits in potentially illegal ways – prompted large investors to sell off their FTX-issued tokens, known as FTT. With nowhere to turn and losses mounting, Bankman-Fried filed for Chapter 11 bankruptcy last week, setting off a cascading effect that has hammered Silicon Valley venture firms and start-ups that depended on FTX. Other crypto exchanges soon after found themselves at risk, with their own assets tied up in the fallout.

On Capitol Hill, the fiasco quickly captured unexpectedly wide, bipartisan attention.

The shift began Tuesday, as lawmakers sorted out the repercussions of the 2022 elections. At a news conference normally reserved for Democratic leaders to lob political barbs and issue policy announcements, Rep. Hakeem Jeffries (D-N.Y.), the caucus chair, said the party had plenty of priorities in the waning weeks of the year – and “the situation related to the cryptocurrency industry will be one of them.”

The House Financial Services Committee, led by Rep. Maxine Waters (D-Calif.), later announced its plans to hold a hearing on FTX, potentially featuring Bankman-Fried’s testimony. “Unfortunately, this event is just one out of many examples of cryptocurrency platforms that have collapsed just this past year,” lamented Waters, describing an “urgency” to act.

Across the Capitol, the fallout from FTX quickly overshadowed what normally might be a somnambulant hearing in the Senate Banking Committee about credit unions. Sen. Patrick J. Toomey (Pa.), its soon-retiring top Republican, seized on the moment to highlight “several high-profile collapses of crypto companies, including one prominent example last week” – a reference to FTX, if not explicitly by name.

Toomey previously has purchased cryptocurrency assets, his personal financial disclosures show. But he focused his opening statement on the repercussions when a firm like FTX, which was based in the Bahamas, can run roughshod over the U.S. economy.

“As a general matter, the failure of Congress to pass legislation in this space and the failure of regulators to provide clear guidance has created ambiguity that has driven developers and entrepreneurs overseas,” he warned. “And we’ve just once again seen how that ends.”

In recent years, Democrats and Republicans at various turns have tried to regulate cryptocurrency, introducing a range of measures to empower federal agencies and pursue abuses, including fraudulent coin offerings and international money laundering. They’ve also held a number of major hearings, even grilling Facebook CEO Mark Zuckerberg in 2019 over his company’s doomed crypto effort, known as Libra.

Law-enforcement agencies, meanwhile, have prosecuted some of the worst actors – unveiling charges in August, for example, against 11 individuals allegedly involved in a $300 million pyramid scheme. And President Biden himself recently has been engaged, signing an executive order in March that offered an early road map for how Washington might approach cryptocurrency regulation.

But the government at times has faced blowback for acting too aggressively. This March, for example, a bipartisan group of lawmakers known as the Congressional Blockchain Caucus took aim at the Securities and Exchange Commission over its attempts to “gather information from unregulated cryptocurrency and blockchain industry participants.” Its signatories included Rep. Tom Emmer (R-Minn.), a caucus co-chair who has argued in the past that the SEC has misused its authorities to assert jurisdiction over cryptocurrency.

Emmer is set to serve in a key House leadership role under a Republican majority next year. Appearing at an industry conference on Wednesday, the GOP lawmaker urged Congress not to adopt a “wet blanket” of regulation in the wake of the FTX crisis.

“We need to use the stage that is Congress to promote all of you beyond the walls of the Capitol,” added Emmer, whose comments were first reported by the publication CoinDesk. “People need to understand more out there that they shouldn’t be afraid of this.”

His office declined further comment.

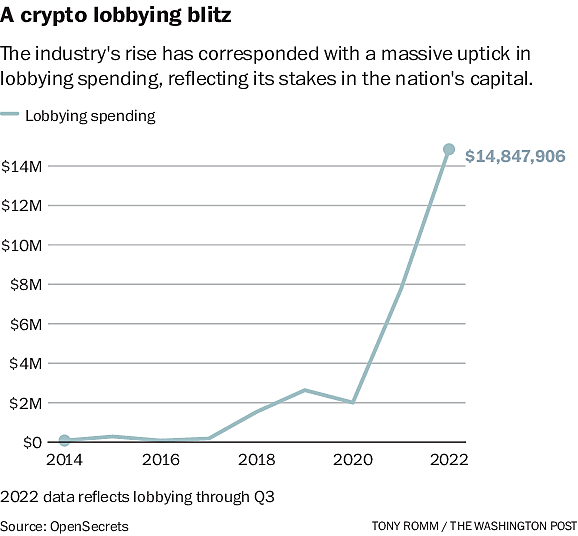

Adding to the challenge, the government has faced an onslaught of lobbying from an increasingly powerful and profitable industry.

Since January alone, cryptocurrency exchanges and their advocates have spent more than $14.8 million to influence regulators and lawmakers, according to lobbying data compiled by OpenSecrets. Bankman-Fried and other FTX leaders, including Ryan Salame, the company’s co-chief executive, also donated more than $70 million in the 2022 election, the analysis showed. That made them the third-largest contributor in the two-year cycle, OpenSecrets found.

“The Senate has trouble keeping up with things that lobbyists prefer the Senate not keep up with,” said Sen. Elizabeth Warren (D-Mass.), a veteran of the 2008 financial crisis, after which she oversaw congressional efforts to keep watch over big banks. Reflecting on the reasons for congressional inaction, she added: “I have said for a very long time now that we need better regulation in this space.”

On Capitol Hill, FTX and its lobbyists actively guided lawmakers in writing legislation that would govern the company and its industry rivals. A regular in Washington, Bankman-Fried personally provided input to Sens. Debbie Stabenow (D-Mich.) and John Boozman (R-Idaho), who introduced a bill this year that would shift some crypto oversight to the Commodity Futures Trading Commission.

The CFTC regulates complicated financial instruments known as derivatives, as well as futures contracts for agricultural products. The crypto industry generally prefers that agency over the SEC, which governs stock and bond markets and is perceived as more aggressive. Lawmakers and administration officials have split over which regulator should have jurisdiction, partly a reflection of the complexity in defining crypto assets – whether they are commodities or securities – under law.

As she raced to a Senate vote this week, Stabenow acknowledged she had solicited feedback from “all the stakeholders … including Sam” on cryptocurrency regulation. A beneficiary of more than $20,000 in campaign donations from Bankman-Fried this election, the senator added she was “extremely surprised, of course – we all were extremely surprised and disappointed” at the downfall of FTX.

But Stabenow still stood by her legislation as an antidote to the risk and abuse seemingly rife in cryptocurrency: “That’s exactly why we need our legislation, so the CFTC can proactively provide regulation and transparency to consumers.”

Other lawmakers, though, feared that the bill had become tainted by FTX’s influence. Brown, the leader of the Senate Banking Committee, specifically acknowledged “concern” that Bankman-Fried and his industry allies had too great a hand in shaping the legislation, noting it “needs major improvement.”

“I think you look at any of the legislation, any legislation written here, (and it’s) always the fingerprints of the big banks. In this case, the big crypto companies are always all over it,” Brown continued. “That’s the fight I make every day in this committee, and it’s the fight we’ll make on this.”

As the FTX collapse rippled through the crypto world, the Biden administration urged Congress to act. On Wednesday, Treasury Secretary Janet L. Yellen issued a public warning about dangers to the economy as she called on lawmakers to fill in the remaining regulatory “gaps.” She said the agency’s prior reports had identified a wide range of “risks” that ultimately were “at the center of the crypto market stresses observed over the past week.”

Behind the scenes, top Treasury officials have been in close contact with major cryptocurrency exchanges and other companies in recent days to assess the FTX fallout, according to an aide who spoke on the condition of anonymity to describe the conversations. Some lawmakers, meanwhile, signaled they were exploring a raft of new proposals in the hopes of protecting Americans who buy, own and sell cryptocurrency.

Sen. Ron Wyden (D-Ore.), a tech expert and leader of the tax-focused Senate Finance Committee, said in an interview that he planned to put forward a “consumer protection package” targeting cryptocurrency in the coming days. The lawmaker worked with other Democrats and Republicans last year in instituting the first-ever tax reporting requirements for digital tokens.

Sen. Mark R. Warner (D-Va.) said this week he had “tried to reserve judgment” given the promise of the technology. But the lawmaker, another top member of the Banking Committee, stressed “there’s a reason we have rules around investor and consumer protection, safety and soundness, and the prevention of financial crime.”

As she left the Tuesday banking hearing, Sen. Cynthia M. Lummis (R-Wyo.) similarly stressed that the FTX meltdown left Congress no choice but to legislate. Lummis, who once took to the Senate floor to “thank god for bitcoin,” has put forward her own, sweeping bill that would shift more oversight to the CFTC.

“I think it’s really important now that senators really focus on digital assets,” she said. “In the past, it’s been easy to put that on the back burner and address other issues that were more front-burner issues. This is now a front-burner issue … We have put ourselves at a regulatory disadvantage.”

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.