When the price of oil seemingly stepped through the looking glass Monday and tumbled into negative value, it summoned up an image of the world of petroleum turned wrong-side-round.

In theory it meant that sellers would have to pay buyers $40 or more just to take a barrel of what used to be called Black Gold off their hands.

It was fleeting, and symbolic, more than anything, and it won’t have much effect on the price of gasoline at the pump. But it also showed just how much the coronavirus pandemic has crushed the world’s energy markets – and how the global effort to stabilize them is failing.

But the notion that a barrel of oil could be worth less than zero was a shock to many.

It was a vivid symptom of the ailments of the oil business, which will probably hit American oil producers the hardest. The oil giants of Saudi Arabia and Russia are state-run conglomerates, capitalizing on cheap oil and able to put national policy ahead of profits if need be. Monday’s price was a warning to American companies that the markets they supply are rapidly deflating.

It comes even as major oil companies have cut back spending on new wells by 30% to 50%, and oilfield service companies have been laying off more and more workers. Some companies have started to shut in their wells, taking a serious hit to their finances.

The negative price recorded Monday was in one sense a short-term anomaly, according to analysts with S&P Global Platts, a commodities analysis firm. It had to do with a specific supply of oil – West Texas Intermediate – and was tied up with the closing of the contract period for May delivery of oil at a time when few need more petroleum.

The Washington Post

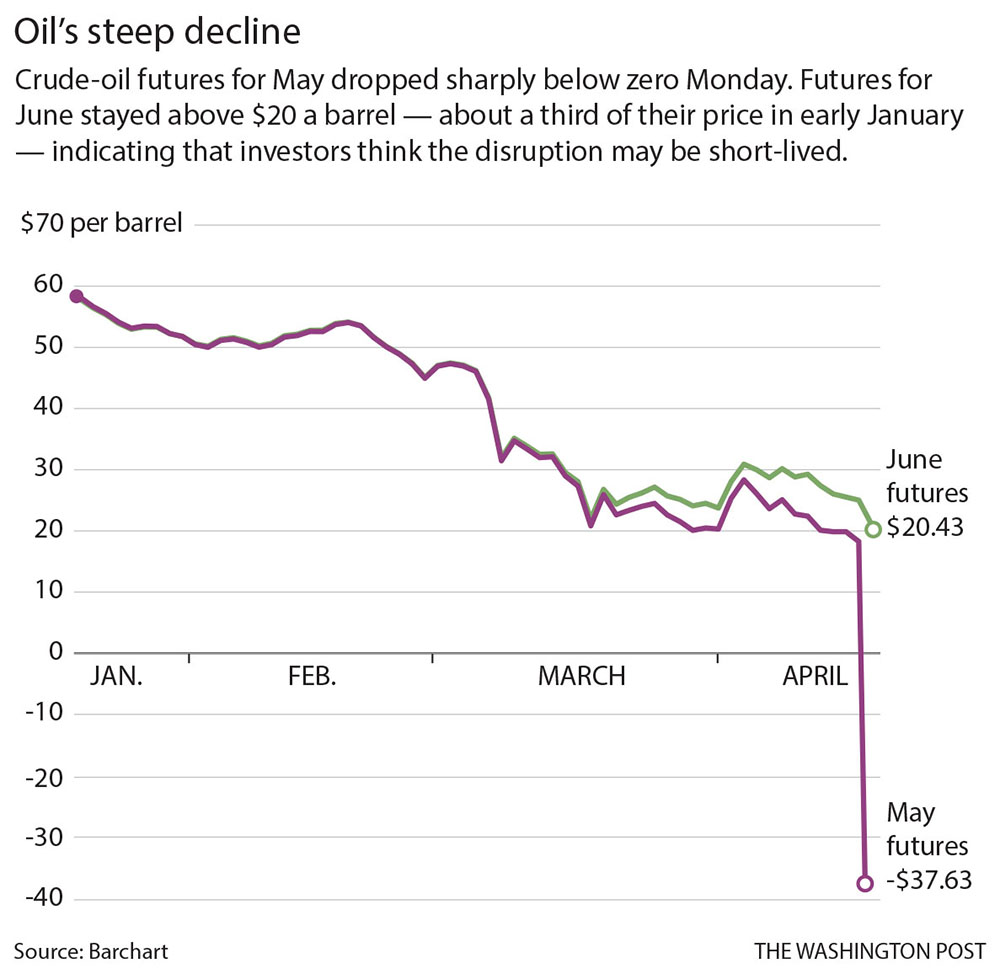

The June delivery price for oil was up slightly Monday, to just over $20. That means that by late spring, traders are betting that oil will still have some value.

Yet even if that June price holds steady – it was hovering around $20 Monday – it is still down about 65% this year, and over time it would devastate North American shale and sand tar companies.

“Whether June contract is fairly priced or has downside, the price is TERRIBLE,” tweeted Abhi Rajendran, of the Center on Global Energy Policy at Columbia University. “Time to wake up to the possibility of 2-3 (million barrels per day) or more of US oil supply gone in a month. Could be talking about 3-4.”

An economist at the University of Notre Dame doubts that that June price will hold steady. The June and July futures prices reflect increased demand for gasoline and jet fuel, said Gianna Bern, but she noted that demand in the transport sector is “at a standstill.”

“In the coming days,” she said, “I think we could see a weak WTI June contract.”

Few want oil in May because there is hardly anywhere to put it. That’s why speculators who held contracts for May delivery – contracts that in a normal month they would have sold to refineries at the last minute – were left with few options Monday but to swallow the losses. One factor not reflected in the tumbling price, though, is that trading was light throughout the day.

Starting in January, the pandemic led to a gradual and then sudden shutdown of the world economy, so that demand is now an estimated 25% to 30% below what it was. But oil-producing nations kept pumping through March and into early April as the Saudis and Russians tried to bluff each other into cutting production, and storage capacity has neared the brink. What little is left has been tied down with leases.

On April 12, both sides, together with the other main members of the Organization of the Petroleum Exporting Countries, agreed to cut production by a purported 10 million barrels a day, or about 10% of global output. But that still is less than the decline in consumption, and stocks have kept growing.

“This moment is of course historical, and could not better illustrate the price-utopia that the market has been in since March, when the full scale of the oversupply problem started to become evident but the market remained oblivious,” Louise Dickson of Rystad Energy wrote in a note. “Since then traders have sent prices up and down on speculation, hopes, tweets and wishful thinking. But now reality is sinking in.”

That agreement was hailed by President Trump as a victory that would right the price of oil and save American oil-related jobs.

Worsening the pain for American producers is a small fleet of tankers leased by the Saudis before the price war was called off and heading to the United States loaded with Saudi crude, according to reports. It would represent seven times the usual amount of oil that Saudi Arabia ships here in a typical month, and it comes even as the United States, which had regained its status as an oil exporter last year, has seen its export markets crumble.

“Today’s collapse poses a devastating threat to our oil and gas sector, with job losses in the thousands and national security being weakened if the industry cannot recover,” Sen. Kevin Cramer, R-N.D., said in a statement issued by his office Monday. “The dramatic low underscores why we cannot allow Saudi Arabia to flood the market, especially given our storage capacity dwindling. Right now, the highest number of Saudi oil tankers in years is on its way to our shores. Given today’s news, I call on President Trump to prevent them from unloading in the United States.”

North Dakota is a major oil producing state, sitting atop the Bakken shale formation, but the break-even price there is as much as $45 per barrel.

Nothing like this happened in the worst of the Depression, or in the early years of the Civil War, the two previous low points for petroleum, according to Bob McNally, head of the Rapidan Energy Group.

Canadian oil companies, which were not parties to the OPEC-Russia agreement, have started to shut in the wells in the sand-tar regions of Alberta. There, too, oil was trading in negative amounts Monday.

“Shutting-in production is a very painful decision for an operator to make – often the economics support running a well at a loss for a certain period of time rather than shutting down the project completely,” said Teodora Cowie, senior oil market analyst at Rystad Energy. “But with infrastructure constraints, this is no longer an option for many landlocked producers.”

“The market is starting the painful process of balancing supply against a smaller demand outlook of about 70 million bpd,” wrote Reid Morrison, an energy analyst with PwC. “The economic situation is locked up with no real clarity about what lies ahead, so there’s no reason to expect demand to increase over the near term.”

Copy the Story LinkComments are not available on this story.

Send questions/comments to the editors.