More women than ever are single, a new report says – and that has significant implications for the U.S. economy.

Single women — who are postponing marriage or forgoing it altogether — are a growing economic force, accounting for a larger share of growth in the job market, homeownership and college degrees, according to an analysis of federal data.

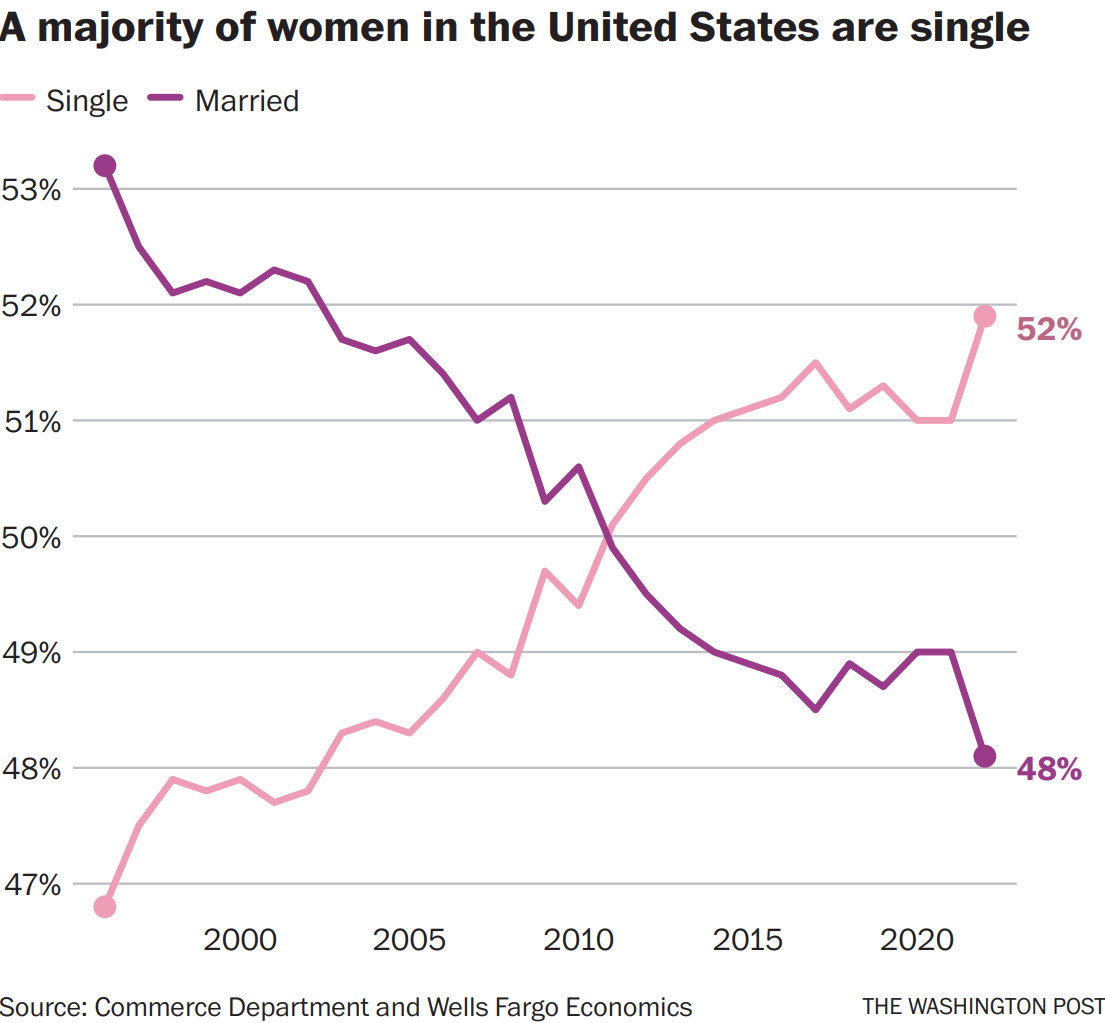

The majority of women in the United States, a record 52%, were unmarried in 2021, according to a report released Wednesday by Wells Fargo. Among the factors driving the rapid rise in single-women households over the last decade: A 20% increase in the number of women who have never married.

But while decades of changing norms around marriage and work have empowered women to carve their own paths, a stubborn wage gap continues to keep many women, especially single mothers, from enjoying the same economic gains as single men and married couples. Never-married women earned just 92% of what never-married men did last year, and have 29% less wealth, Wells Fargo economists found.

“The sheer growth of single women is rippling across the economy and leaving a mark on the labor market, wealth and spending,” said Sarah House, senior economist at Wells Fargo and lead author of the report. “The bad news, though, is that the wage gap [between men and women] has remained stuck over the past 15 years. Single women are filling a void in a very tight labor market, but they are still earning less than single men.”

Women have made strides in just about every facet of the economy in recent decades. The number of women attending and graduating from college has outpaced men for years, according to government figures. Women are also more likely to buy their own homes, despite lower wages. Nearly 11 million single women owned their homes in 2021, compared with 8 million single men, according to a recent analysis of census data by LendingTree.

After Alicia Barnes got a divorce in 2009, it took a decade for her and her young sons to regain their financial footing. Barnes, a Navy veteran in Oakland, Maine, says she was “grossly underpaid” for years, making $37,000 a year as an advertising analyst in an industry where the average annual pay is well over $65,000, according to ZipRecruiter.

Now Barnes, 48, works as a digital strategist on a political action committee that campaigns for health care reform, where she makes nearly six figures and has good benefits, including a robust 401(k) match. She recently bought a $276,000 house for herself and her sons, now 18 and 22.

“This is the first time I’ve had employment that pays me what I’m really worth,” Barnes said.

Women are also more likely to live alone than in the past – whether they own or rent. Households helmed by single women now make up 26% of U.S. households.

Growing up, Rebecca Lundberg figured she would be married by now. But at 31, she says she is happily single – and thriving. She makes $90,000 a year at her Washington, D.C., marketing job and has been renting her own place for five years.

“We’re one of the first generations that’s not really worried about getting married in our 20s and 30s, even our 40s, because we have the means and opportunities to live our own lives,” she said. “Being in charge of my own personal and financial decisions, and having my independence is very liberating for me.”

Lundberg says she meets people on dating apps or through friends, though it’s been difficult to forge a meaningful relationship in a sea of working professionals. About half of her friends are married, though the rest are single and “just kind of living city life.”

“I’m not necessarily looking for marriage in the near future, but it would be nice to occasionally not have a date ghost you,” Lundberg said. “If you give any hint that you might be looking for something even halfway serious, you just don’t hear from people again.”

Marriage has long been the most prevalent household arrangement for women and has often served as a vehicle for higher earnings and wealth. While single men out-earn single women, married couples had nearly four times the median net worth of single people in 2019, according to the Federal Reserve.

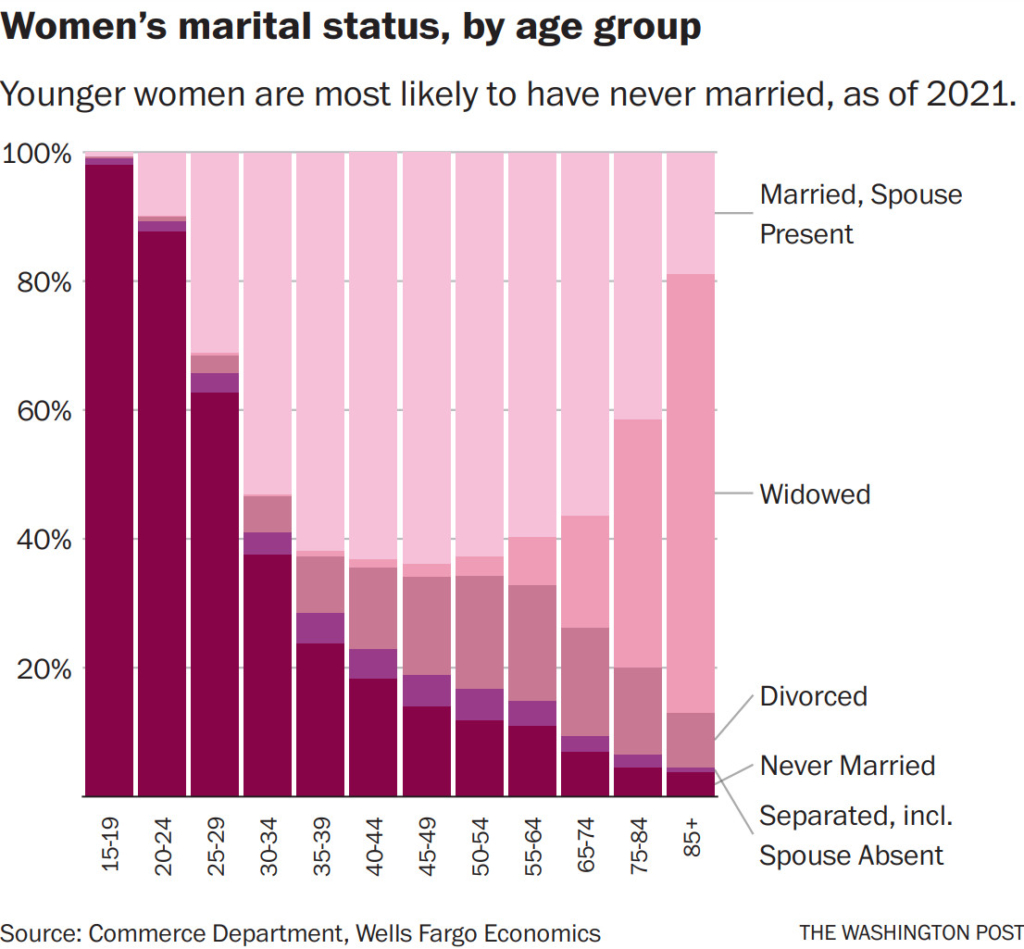

Economists say those discrepancies are particularly concerning as more people put off marriage for longer periods of time. The median age of first-time marriage for women has steadily risen, from 25 in 2001 to 28 in 2021.

Single women – whether divorced, separated or never married – are more likely to be working than married women. The share of never-married women who are working or looking for work has risen nearly two%age points in the past decade, even as the overall labor force participation rate has declined.

But their lower wages mean they have less spending power. Single women spent an average of $39,000 in 2021, compared with $41,000 for single men. But their buying patterns were considerably different: Women were more likely to spend on basics such as housing, health care and education than on entertainment, travel and dining out.

“Single women tend to have less wealth – and that’s particularly true if they’re single mothers,” House said. “Overall, given their lower income, more spending goes to necessities.”

Children can weigh heavily on single mother’s wealth, House and her team found. Single women with children had a median net worth of just $7,000 in 2019, compared to $65,000 for single women without children.

(It was a different story for single men: Those with children sacrificed just $2,000 of their overall wealth.)

Years of depressed pay can make it difficult for women to build a financial safety net or save for retirement. The result, Wells Fargo economists write, is that “single women often remain in a more financially fragile position than other segments of the population.”

For decades, Kimberly Jimenez, 60, had a well-paid jobs at major law firms. She owned a house in Lake Elsinore, Calif., and made more than $80,000 a year. But after being laid off in 2005, she took on a part-time job that paid less than half of that – $30,000 a year – doing insurance work from home. Two years ago, that dried up too, leaving her with few options. She borrowed against her home, began selling postcards and sheet music on eBay, and started relying on food stamps to make ends meet.

“I ended up being in a role that my mom found herself in, that I never thought I would be: Not being able to support myself financially,” she said. “That was something I never, ever envisioned for myself. I was raised a feminist to take care of myself, to not have to depend on a man for my income.”

Jimenez, who is in physical therapy for car accident injuries, says she is hoping to get back into the workforce soon. She plans to focus her search on remote jobs.

“I’m resourceful, I know I can make it work,” she said. “But it’s a reminder that we can be way up here, doing really well one minute and it just takes one thing, one occurrence, to destroy it all.”

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.