One of the unintended consequences of the Federal Reserve’s long battle against inflation is the current turmoil in the financial system that led to the biggest bank failure since the Great Recession.

The collapse of Silicon Valley Bank, Signature Bank as well as the last minute private-sector rescue of First Republic all have roots in the Fed’s move to sharply hike interest rates to tamp down surging inflation. Although there’s lots of blame to go around.

That puts the Fed in a very difficult spot this week as officials meet to figure out what level of interest rate hikes can continue to bring down inflation without wrecking the banking system. They have to manage dual threats to the economy – inflation and banking stability.

How exactly did we get here? Here, in seven charts, is a look at how the Fed’s fight against high prices helped trigger instability in the banking sector.

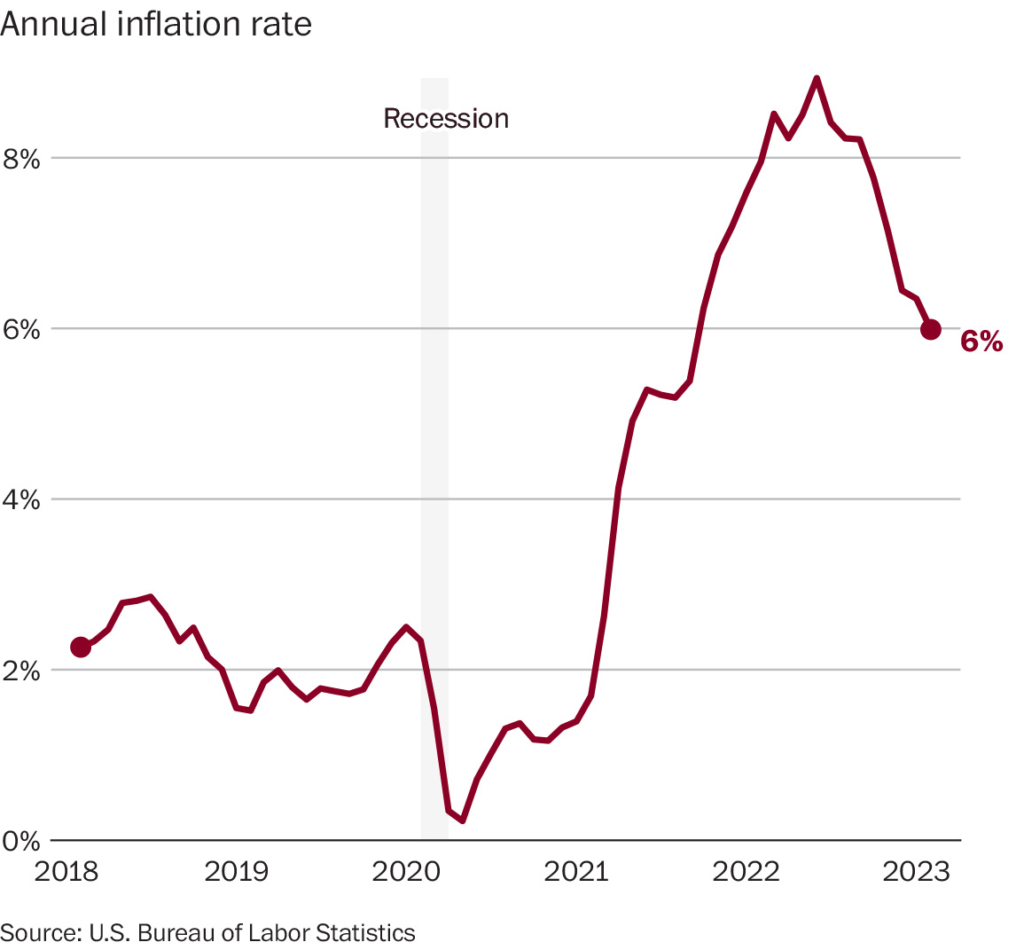

PRICES BEGAN RISING EARLY IN THE PANDEMIC – AND KEPT GOING

The economy all but came to a standstill when covid took hold in March 2020. More than 20 million workers lost their jobs. Schools, restaurants, gyms and countless other businesses shut their doors. Everybody was ordered to stay home.

As a result, the economy plunged into a steep recession.

By the time things opened back up – and people began spending again, armed with new stimulus funds – there were major shortages, supply chain snarls and production hiccups that stoked inflation. Demand for goods skyrocketed, while supply remained depressed. The result: higher prices.

But the Fed didn’t act. Policymakers, including the president, were adamant that the inflation was temporary and would sort itself out once pandemic-related shocks calmed down.

It wasn’t until December 2021, when inflation hit a 40-year high of 6.8 percent, that Fed officials began talking about raising interest rates. They finally did so – by a modest quarter percentage point – in March 2022. By then, prices had risen a whopping 9 percent from the previous year.

FED TRIED TO CATCH UP BY AGGRESSIVELY RAISING INTEREST RATES

Since then, the central bank has raised interest rates seven more times, with the goal of slowing the economy enough to curb inflation.

But a number of new complications – including the war in Ukraine, which led to higher gas and energy costs – forced the Fed to double down on its efforts. Each jump in interest rates dealt a shock to the economy, though it wasn’t immediately clear what the end result would be.

FED’S ACTIONS LED TO HIGHER BORROWING COSTS

The central bank controls just one interest rate: The federal funds rate, which is what banks use to lend money to each other overnight.

That rate has skyrocketed from near zero to roughly 5 percent in the past year, the fastest increase on record.

And it doesn’t take long for banks to pass on those higher borrowing costs to customers: Mortgages, business loans and other types of lending have all gotten more expensive in the past year.

BOND MARKET SEES BIGGEST DECLINE ON RECORD

Bonds, which are loans to a company, or in this case the government, typically pay fixed interest rates and are seen as safe and reliable investments.

And while the Treasury Department always issues a lot of bonds, it has issued even more in the past 10 years, because that’s how the U.S. government finances pricey projects. Trump tax cuts. Pentagon budget. COVID-era stimulus programs to prop up the economy under Trump and Biden.

But as interest rates climbed, investors were more interested in new bonds that promised to pay more, and long-term bonds tied to older, lower rates, became less desirable – and therefore less valuable.

As a result, the bond market took a nosedive last year, notching its steepest decline.

BAD NEWS FOR BANKS LIKE SVB, WHICH INVESTED HEAVILY IN FIXED-RATE BONDS

In recent years, banks – newly flush with extra deposits from pandemic-era savings and stimulus – bulked up on bonds and other fixed-rate investments like mortgage-backed securities. At SVB, fixed-rate securities made up nearly 60 percent of the bank’s assets at the end of 2022.

But as the Fed raised interest rates, those bonds became less valuable. SVB’s $91 billion portfolio of long-term securities was worth just $76 billion at the end of 2022. That $15 billion gap was far wider than the $1 billion shortfall the company reported a year earlier.

In addition, the vast majority of the bank’s deposits – nearly 94 percent – were uninsured, according to data from S&P Global. The national average is about half, which left SVB especially vulnerable to fears of a run that became self-fulfilling. The bank’s customers withdrew $42 billion in just 24 hours, leaving the bank with a negative balance of $1 billion.

“It’s simple: When interest rates go up, the value of bonds go down,” said Darrell Duffie, a management and finance professor at Stanford University. “Silicon Valley Bank had a whole lot of bonds – both treasury securities and mortgage bonds – so when the Fed raised interest rates to try to reduce inflation, the value of all of those bonds went down.”

That wouldn’t have been a big deal if SVB had been able to hold onto its bonds until they matured. But with a rush of depositors clamoring to take their money from the bank, SVB had no choice but to sell its securities at a massive loss. The bank quickly collapsed.

“It was a classic bank run,” Duffie said.

COUNTLESS OTHER BANKS ARE SITTING ON BILLIONS IN DEVALUED TRESURIES

SVB wasn’t alone in its stockpile of depreciating bonds. U.S. banks are sitting on a staggering $620 billion in unrealized losses, according to the FDIC.

The Federal Reserve last week stepped in with an emergency program that allows banks to trade in devalued bonds for their original value in cash. While this offers a temporary fix, economists say there may be other unforeseen issues lurking in the financial sector.

“So far, we’ve been able to prevent big spillover effects – the central bank and others have come in with rapid solutions to keep this from metastasizing into a broader banking crisis,” said Dana Peterson, chief economist at the Conference Board. “But there could still be more shoes to drop.”

The Fed has moved quickly to stem a broader financial crisis, launching a new emergency lending program with generous terms to complement its existing “discount window” for emergency loans. The measures are so far gaining traction, with banks borrowing at the window hitting an all-time high of $153 billion last week.

WHAT’S NEXT?

The whirlwind events of the past week and a half have raised new questions about the Fed’s next move.

The European Central Bank last week stuck with its aggressive plan to hike interest rates by half a percentage point for the euro zone, despite troubles for the Swiss behemoth, Credit Suisse, that required the bank to borrow up to $54 billion from the Swiss National Bank.

Many experts and investors still expect the central bank to hike interest rates by another quarter-percentage point when it meets Wednesday, though there are growing concerns that the financial system may be too fragile to handle the higher rate.

That is a sharp turnaround from earlier this month, when Fed Chair Jerome H. Powell laid out the option of boosting interest rates by half a percentage point, citing stronger than expected readings on inflation and employment. The economy added more than 800,000 jobs in the first two months of this year and inflation remains high, with prices up 6 percent from last year.

But all of that is now in the rearview mirror as investors worry about the potential cascading effects of bank failures and increased market stress.

“The Fed still wants to raise rates a bit more,” said David Donabedian, chief investment officer of CIBC Private Wealth US. “It’s just a matter of whether the banking system volatility will let them.”

Send questions/comments to the editors.

Comments are no longer available on this story