WASHINGTON — A sharp rise in gas prices and inflation, combined with turbulence in the job market, are creating new economic pressures for President Biden just as he tries to secure a legacy-defining set of domestic spending proposals.

The Washington Post

Over the past week, the Biden administration has been met with disappointing economic benchmarks, including lackluster hiring and a surge in consumer prices. Meanwhile, rising gas prices and fuel shortages have hammered the Southeast. These pressures have weighed on the financial markets, as the Dow Jones industrial average and the S&P 500 fell sharply for the third day in a row.

So far, the White House has largely responded to these setbacks by either downplaying them or arguing that they amount to one-time aberrations related to the unusual circumstances tied to the rebound from the coronavirus pandemic. In some cases, the White House has said indicators such as a rebound in prices in the travel or hospitality industry reflect an economy beginning to return to health.

However, the head winds have galvanized Republican complaints about the administration’s economic stewardship and its $1.9 trillion stimulus package at a pivotal moment for the president’s domestic agenda. The White House is this week holding meetings with senior congressional leaders as it seeks progress on its $2.3 trillion jobs and infrastructure package, while simultaneously seeking to approve another $1.8 trillion in additional domestic spending priorities. The latest economic tremors may try the White House’s willingness to aggressively press major new policy changes.

Advisers close to the Biden administration describe the current juncture as a key test of its commitment to major economic policy change in the face of escalating attacks from business groups and the GOP.

“There is anxiety coming out of the White House after Friday’s numbers, but they need to stay focused on tried and true methods to get the economy back on track rather than caving” to GOP demands, said one outside economic adviser to the White House, who spoke on the condition of anonymity to frankly describe internal dynamics.

The administration has already demonstrated its sensitivity to criticisms over its economic agenda. White House officials held a slew of weekend meetings involving the National Economic Council and Department of Treasury to assess how to respond to complaints that the labor shortage was constraining the recovery, two people familiar with the matter said. On Monday, the president emphasized rules limiting unemployment benefits and said the administration would work to reimpose work search requirements on unemployment beneficiaries, while disputing criticism that generous jobless benefits are keeping people out of the workforce.

Former treasury secretary Larry Summers, an early critic of the administration’s stimulus plan, called on the Treasury Department and central bank to go further and publicly acknowledge inflationary risks pose more than a temporary blip.

“Whatever else may have been true several months ago, the preponderant macroeconomic risk facing the U.S. today is overheating,” Summers said, citing jumps in prices, reports of labor and commodity shortages, and average hourly earnings data, among other indicators. “If inflation expectations are allowed to ratchet up – which certainly appears to be a real possibility – the costs economically and politically could be very high.”

Administration officials have maintained that America is on pace for a rapid recovery and that the recent tremors reflect the growing pains of a long dormant economy snapping back into shape. White House economist Jared Bernstein said the administration has long expected a temporary bump in inflation as demand surges in certain sectors and as economic normalcy returns, particularly compared to the steep declines around this time last year.

“There’s always going to be a great deal of noise around the data at a time like this,” Bernstein said in an interview. Some economic data “will come in hot; some will come in cool; but you have to keep your eye on the bigger picture and the context of an economy building back to strength.”

Asked if the news would lead the administration to reconsider its economic agenda, Bernstein said: “Not at all. If anything, what we’re seeing are the positive impacts of the rescue plan as they work their way through the recovery . . . The most fundamental observation of this price report is that people are reengaging with sectors that were hit terribly hard. That’s good for those business; that’s good for those families.”

However, critics see signs of economic disarray emerging in numerous places simultaneously that should give the administration fresh pause.

Stocks fell sharply Wednesday, extending Wall Street’s losing streak to three days, after showering investors with a series of all-time highs amid vaccine rollout optimism. The Dow Jones industrial average shed nearly 682 points or 2%, to close at 33,587.66. The S&P 500 gave up 89 points, or 2.1%, to close out at 4,063.04.

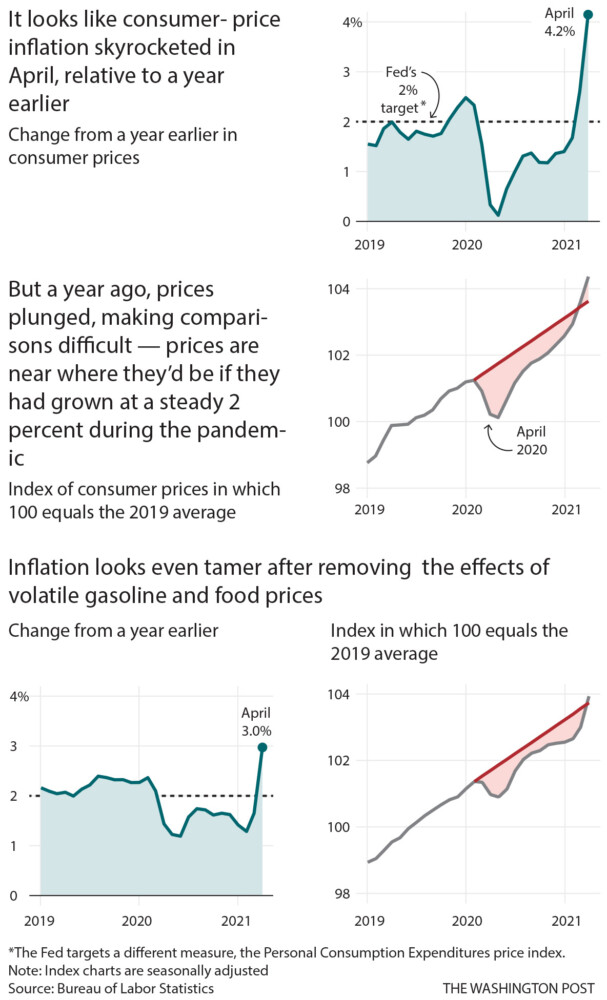

Markets fell in part on the news from the labor department reporting that consumer prices surged 4.2% higher in April compared with a year ago, stoking concerns of an overheating economy and rising inflation. The April hike in consumer prices was the highest since the Great Recession, driven by federal stimulus checks as well as widespread vaccinations that helped kick-start people’s demand for goods and services, before supplies could catch up.

Some of the most significant price increases came from used cars and trucks, which rose 10% in April. That’s the largest one-month increase in almost 70 years, accounting for over one-third of the seasonally adjusted rise in prices for all items, according to the Bureau of Labor Statistics. The cost of shelter, airline fares, recreation, motor vehicle insurance and home furnishings also drove April’s overall price climb. Lumber and other sectors have been unable to keep with demand, creating “bottleneck” effects that lead to high prices.

Some economists caution that the headline increase in prices may be misleading, because inflation is typically measured as change from a year earlier. A year ago, the economy was in an exceptional moment: April 2020s inflation figure was unusually low, thanks to the fast-spreading pandemic and the accompanying shutdowns and crash in consumer spending that came with it. As a result, this April’s number has long been expected to look unusually high, because it’s relative to the nadir of a crisis.

Still, the data included other troubling signs of inflation. Price growth has accelerated every month starting in December, and picked up dramatically between March and April to the fastest level since 2009. The monthly increases suggest inflation is picking up rapidly even when not compared to the lows at the outset of the pandemic.

Federal Reserve Chair Jerome H. Powell said he expects inflation figures to fall in the year to come, as the super-low readings from the pandemic’s early days shift out of the calculation. Federal Reserve officials have said prices should simmer back down as the economy recovers, although at least one Fed official noted the intensity of the price increases.

“I was surprised,” Federal Reserve vice chair Richard Clarida said Wednesday. “Obviously we have pent-up demand in the economy – it may take some time for supply to move up to the level of demand.”

Price jumps hit the country in a particularly visceral fashion this week as the shutdown of the Colonial Pipeline due to a ransomware attack disrupted daily lives of commuters and sparked fears of gasoline shortages on the Eastern Seaboard.

Close to 30% of North Carolina’s fuel stations were emptied, and gas stations saw surges in demand in multiple states, including as far north as Maryland and Delaware. Average gas prices breached $3 per gallon for the first time in about seven years, with some reports emerging of gas prices as high as $6.99 per gallon.

Colonial has reported progress and the administration has said a full resumption of service is expected by the end of this week. Yet the alarm put the White House on the defensive as it seeks to push through a major overhaul of the U.S. energy sector. House Minority Leader Kevin McCarthy, R-Calif., slammed Biden over gas, car, and lumber prices on Wednesday.

The anxieties over the gas shortage and inflation come on top of the April jobs report, released Friday, which showed an unexpected slowdown in the pace of hiring compared to the month before. The president and Treasury Secretary Janet Yellen urged patience and said the economy is still creating roughly 500,000 jobs on average every month. The weak job numbers fueled complaints from business groups that the $300 per week unemployment benefit, approved by Democrats in March, is discouraging workers from returning to the labor market.

Many economists dispute that notion, but the attacks are still poised to threaten the administration’s broader agenda. Republicans were quick to call for the administration to seek either compromise or slow down the pace of the more than $4 trillion in spending it wants to approve over 10 years. Conservatives have long expressed unease about the trillions of dollars approved by Congress in response to the pandemic.

“What we have done over the last year is well beyond what we can point to historical examples to guide us on, so it’s extremely important to take a pause and see how this is all actually affecting the economy,” said Brian Riedl, a former aide to Sen. Rob Portman, R-Ohio, now at the Manhattan Institute, a libertarian-leaning think tank. “The experts have been getting it wrong; they severely underestimated both the jobs and inflation data. So it’s vitally important to respond to events and reevaluate.”

But the administration faces competing pressure not to shrink its proposals in the face of GOP opposition. Rep. Pramila Jayapal, D-Wash., chair of the Congressional Progressive Caucus, said that the jobs numbers bolster the case for the White House to push for major investments in child care, pointing to the decline of employment among women. Jayapal circulated a letter on Wednesday signed by 60 House Democrats, including some centrists, saying that “the pursuit of Republican votes cannot come at the expense of limiting the scope of popular investments.”

“The White House should not be scared,” Jayapal said in an interview. “I understand the White House is getting hit by Republicans on this, but to me the way to deal with it is to lean in to the jobs report, whereas work search requirements and cracking down on people is not the right way to go.”

Send questions/comments to the editors.

Comments are no longer available on this story