Maine’s highest court last week turned the state’s foreclosure law upside-down with a decision it says corrects a “draconian” rule that likens courts to casinos by handing out free houses.

But foreclosure defense attorneys say the ruling weakens one of the few protections in place for homeowners facing foreclosure and threatens the standing of other precedent-setting cases.

In Maine, to foreclose on a property, a lender must first send a notice of default, which lays out what the borrower owes and how to get up to speed on the loan. State statute has strict requirements for what must be included in the notice.

The borrower then has 35 days to “cure” or become current on their balance before the lender can “accelerate” or demand full repayment of the loan and file a foreclosure suit.

Because of the statutory requirements for these letters, any mistake or “defective” notice of default essentially costs the bank the lawsuit. And following landmark cases like Pushard v. Bank of America – decided unanimously by the state supreme court in 2017 – and the legal principle known as res judicata, the mortgage is deemed unenforceable, and banks can never file a foreclosure suit on that property again. It also means the mortgage is discharged and the borrower, in effect, now has a free house.

Last week, in Finch v. U.S. Bank, N.A., an almost entirely new Maine Supreme Judicial Court issued a “course correction” and ruled 4-3 that when a lender fails to comply with the requirements of the default notice prior to initiating a foreclosure action, the lender does not lose the right to subsequently enforce the mortgage. In so doing, the court overturned its prior precedent in the Pushard case.

The majority criticized this “court as casino” foreclosure process that they called “disproportional” and “draconian.”

“A single typographical error in a required notice of default can have the same windfall result as winning a casino bet, but in the form of a house instead of cash,” they wrote. “A ‘free house’ forfeiture, if it is ever decreed, should be reserved for conduct worse than issuing a single defective notice.”

But the notice of default is a crucial step in the foreclosure process, said Jonathan Selkowitz, a mortgage defense attorney with Pine Tree Legal, a nonprofit that provides legal aid to low-income Mainers. It’s one of relatively few protections for homeowners, and it has “completely lost its teeth because of this decision,” he said.

In the cases Selkowitz has litigated, they’re not dealing with a small typo.

In one case, the homeowners owed about $3,000, but the loan servicer claimed they owned closer to $50,000. In other situations, homeowners have received loan modifications from one servicer and then when the loan is transferred, it isn’t honored.

The default letters sent out in the years following the 2008 housing crisis were “terrible,” according to Thomas A. Cox, a Maine foreclosure defense attorney. They were often incorrect or lacking any useful information, they were vague, and it was often difficult to get a hold of lenders for clarification.

But following several cases such as Pushard in the mid-2010s, the quality of those letters turned around. The banks knew they only had one shot to get it right.

“These letters are not difficult to write. The statute is very clear,” he said.

Most of the time, letters are done properly. In the last 10 years, Cox estimated there have been fewer than 200 cases where there have been defense judgments due to defective default letters or other case defects.

“There just are not a lot of cases where the banks do not win,” he said.

But Cox is concerned that the quality of the letters could deteriorate following the recent ruling.

“What I fear is going to happen … is that the banks aren’t really going to worry about these default letters being accurate because if they screw up, eh, they can do it again,” he said.

SOME JUSTICES DISSENTED

Mortgages are bought and sold all the time – a mortgage can change hands multiple times throughout the lifetime of the loan, and Selkowitz said it’s often during these transfers between services that accounting errors happen.

Selkowitz fears banks will be able to use the Finch decision as a “get out of jail free card” in future mortgage service mishandling cases.

“I think what my client community is going to experience is that banks are going to be way less willing to do what we all agree is the goal here, which is to work it out. Everyone is talking about the free house and how draconian that is … but the reality is, that happens very very infrequently,” he said. “Strict protections help me settle cases. Not help people get free houses.”

More often than not, the homeowner either loses, gives up or works it out with the bank, he said. But this decision, he said, limits the lender’s desire to come to the table and work it out.

“They’ll just say, we’ll lose and bring another foreclosure,” he said.

The dissenting justices voiced a similar concern.

If unsuccessful, “the (lender) can simply file another complaint and try again. And again, and again. Until the (lender) is able to get it right. Or until the (borrower’s) ability – financial and otherwise – to resist the claim is expended and exhausted. And all the expense of limited and precious judicial resources,” they wrote. “By fundamentally altering the law to diminish the effect of legally consequential mistakes by (lenders), the court creates a special privileged class of litigant – one whose numbers will no longer suffer the preclusive consequences of a deficient case, unsuccessfully presented.”

Morgan Nickerson, a Boston-based attorney who represented U.S. Bank in the Finch case, said he expects to see fewer foreclosures make it to trial as a result of the decision.

“I think what was happening in Maine beforehand, every counsel for a borrower in a foreclosure action would take the case all the way to trial in hope there would be a misstep,” he said. “Any technical win for the borrower would result in a free house, so there was huge incentive to take it to trial.”

Without that, he said, he expects to see more settlements earlier on in the foreclosure process.

Selkowitz, though, rejected the idea that lawyers push to bring cases to trial.

Whenever there’s an agreement on the table, he said, they try to take it.

“It’s so much safer for them,” he said.

PRECEDENT OVERTURNED

Both parties say the reversal is surprising, given how recently the precedent was set. The 2017 decision was unanimous, while the Finch case was decided by a single vote.

“Usually courts don’t overturn themselves that quickly,” Nickerson said. “The judges really disagreed. I don’t see a lot of 4-3 decisions in Maine.”

Cox agreed and said there was much about the case that defied expectation.

“This kind of a vigorous dissent is unusual,” Cox said. “I see in the dissent a warning to others.”

Justice Andrew Mead and retired Justices Jeffrey Hjelm and Thomas Humphrey dissented, arguing that overturning the recent decision could not only harm homeowners, it could also damage the court’s credibility.

“It does not do so because the law emanating from those cases has become antiquated. It does not do so because the law has changed. Rather, the court does so simply because it now disagrees with the outcome of the cases we decided a short time ago,” they wrote.

This decision, they said, goes well beyond overruling most all of those two 2017 cases, it calls into question other important areas of established foreclosure law.

Attorneys who expressed similar concerns did not outline what other cases might be at risk, but Selkowitz noted that there are still other provisions beyond a defective default letter that could result in the “free house.”

“Even beyond that,” the justices wrote, “the court’s willingness to make an abrupt change in the direction of the law in these circumstances reasonably raises questions about the extent to which this court is willing to adhere to established precedent generally.”

FORECLOSURES STILL LOW IN MAINE

Foreclosure rates across most of the country increased in 2023 but remain below pre-pandemic levels, according to Attom, a California firm that tracks property data by state. Maine, however, is among just a handful of states that saw foreclosure rates drop in 2023.

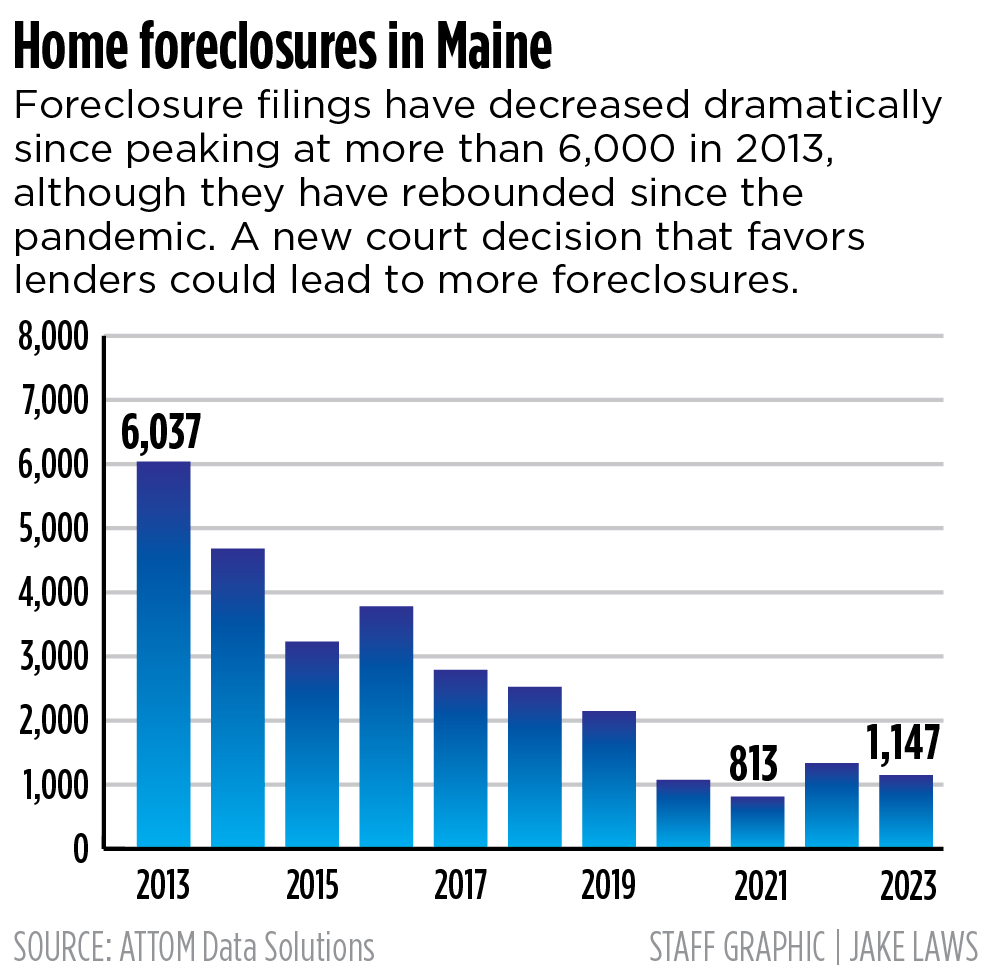

An annual increase was expected. Mortgage lenders locally and nationwide offered forbearance programs to help carry struggling borrowers through some of the more difficult months of the coronavirus pandemic. But now, those programs have ended along with a pandemic-related moratorium on foreclosures. It’s not clear exactly why Maine may be faring better than other states. Overall, Maine has seen a dramatic decrease in foreclosures since peaking at more than 6,000 in 2013. Last year, there were only 1,147.

MaineHousing has, for the last year or so, run a Home Owner Assistance Fund, which provides financial assistance to eligible homeowners of up to $50,000. Applications closed in early January. The money is available to homeowners who saw their income or expenses impacted by the pandemic and can be used to help cover late mortgage payments as well as up to three months of future payments, back property taxes and utility bills. The fund currently has about $11 million remaining of the original $50 million.

Maine’s hot housing market is also giving people more equity in their properties, which might be providing a cushion against foreclosure.

Maine is a judicial state, meaning that the foreclosure is a lawsuit between the bank and the borrower and has to go through the court system. Foreclosure in Maine takes a little over a year, on average, while they take closer to 90 days in a non-judicial state such as New Hampshire.

About 357,000 homes nationwide, or one in every 391 properties, were subject to foreclosure filings in 2023, according to Attom.

In Maine, just shy of 1,150 homes – one in every 643 – had foreclosure filings, ranking the state No.16 among those with the lowest foreclosure rates.

South Dakota recorded the lowest rate, with just one foreclosure filing for every 3,319 homes, according to Attom. Most states saw an increase in foreclosures, many by double-digits.

The new data from Attom show the foreclosure rate in Maine fell about 14% last year compared to 2022. Only Illinois had a bigger decrease.

“Homeownership is not like any other asset,” Selkowitz said. Losing a foreclosure case isn’t just a matter of keeping or losing a house – it can affect a family’s financial standing for a generation.

“The stakes are so high,” he said.

Copy the Story LinkSend questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.